Canada Bank and Credit Card Apps and Websites Perform Well Overall, but Virtual Assistants Struggle With Complex Tasks, JD Power Finds

Bank and Credit Card Digital Platforms Show Solid Fundamentals, but Gaps Emerge in Critical Moments

- Core digital banking and credit card experience remains strong overall

- Comprehensive virtual assistants drive significant increase in overall customer satisfaction

- Virtual assistants strained by more advanced security and customer service tasks

TORONTO: 4 June 2026 — Banks and credit card providers in Canada are steadily expanding artificial intelligence (AI)-powered virtual assistants across their mobile apps, but the technology continues to fall short in high-stakes customer scenarios. While virtual assistants perform well for simple transactional tasks, they struggle to guide customers through more complex issues, according to a series of recent studies of banking and credit card mobile app and online users in Canada, released today.

The studies—the JD Power 2026 Canada Banking Mobile App Satisfaction Study;SM 2026 Canada Online Banking Satisfaction Study;SM 2026 Canada Credit Card Mobile App Satisfaction Study;SM and 2026 Canada Online Credit Card Satisfaction StudySM —track overall customer satisfaction with banking and credit card providers’ digital offerings.

“AI-powered virtual assistants are becoming a more prominent feature across banking apps in Canada, and customers are clearly open to using them for everyday financial questions and simple transactions,” said Jennifer White, managing director of financial services intelligence at JD Power. “But the data also shows a hard ceiling: when situations become complex, especially around fraud or urgent account issues, these systems still struggle to deliver effective resolution. The next phase in the evolution of this technology isn’t about adding more automation but rather designing better handoffs to human support before customers get stuck in frustrating self-service loops.”

Following are some key findings of the 2026 studies:

- Core digital experience remains strong despite AI friction: Overall satisfaction (all on 1,000-point scales) with Canada banking apps is 678; overall satisfaction with banking websites is 668; overall satisfaction with credit card apps is 674; and overall satisfaction with credit card websites is 654. Despite ongoing challenges with virtual assistants, these performances are driven largely by the strength of the core digital experience, as most bank and credit card apps and websites deliver on key fundamentals including fast and seamless login, modern design and intuitive navigation.

- Virtual assistants drive increase in satisfaction when they work well: When users perceive virtual assistants as highly comprehensive and capable, overall satisfaction is 160 points higher than the industry average. However, satisfaction drops when users attempt to resolve problems, dispute charges or identify fraud, exposing a critical gap in handling security and customer service needs and underscoring the importance of deeper functionality and reliable escalation paths to support customers’ needs.

- Virtual assistant users tend to be tech-oriented and younger: Virtual assistant users tend to be younger, more tech-oriented and heavier mobile app users. Usage is concentrated among Gen Z[1] (19%) and Millennials (13%), and as these digital-native users increasingly turn to virtual assistants, expectations continue to rise, putting pressure on providers to deliver more capable and reliable tools.

“When virtual assistants strike the right balance between simplicity and robust capability, they can significantly elevate the digital experience for bank and credit card customers,” said Jon Sundberg, director of digital solutions at JD Power. “At this stage, while many providers have introduced virtual assistant features, few have successfully combined intuitive design with a broad range of functionality. Closing that gap is the next major step for banks and credit card issuers, especially as more customers grow comfortable turning to AI-driven tools for financial guidance.”

Study Ranking

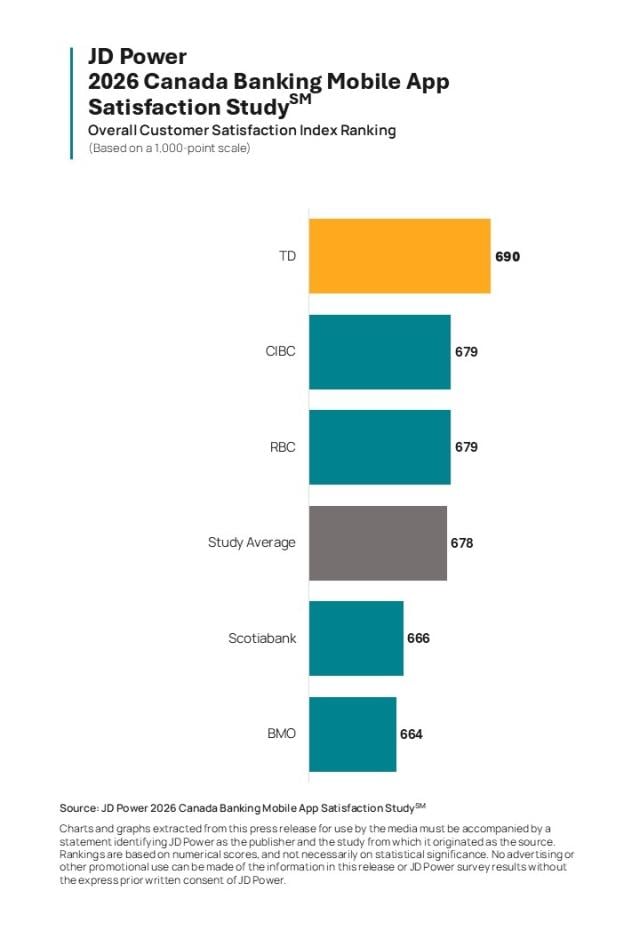

TD ranks highest in banking mobile app satisfaction, with a score of 690. CIBC and RBC rank second, in a tie, each with a score of 679.

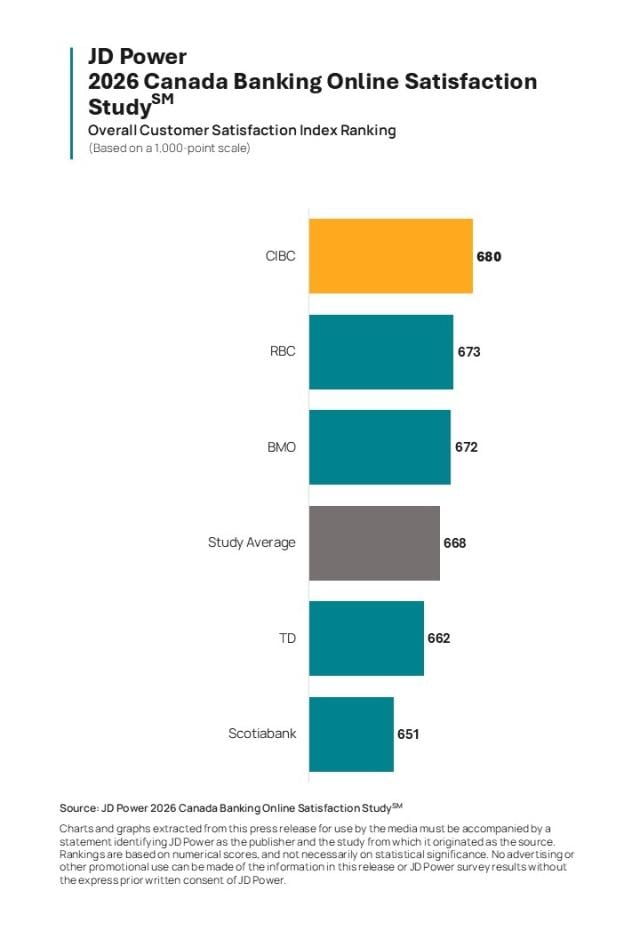

CIBC ranks highest in online banking satisfaction for a second consecutive year, with a score of 680. RBC (673) ranks second and BMO (672) ranks third.

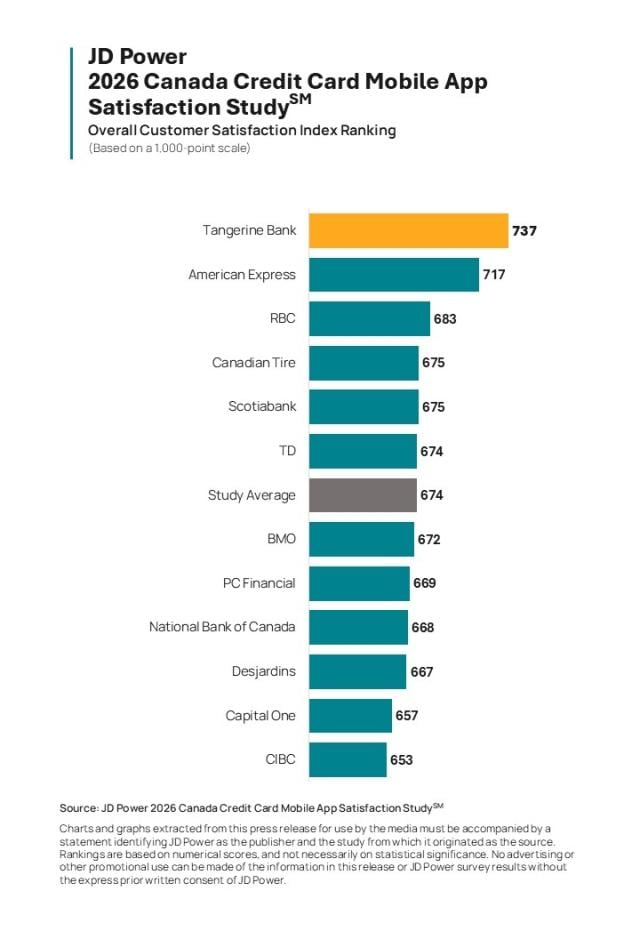

Tangerine Bank ranks highest in credit card mobile app satisfaction, with a score of 737. American Express (717) ranks second and RBC (683) ranks third.

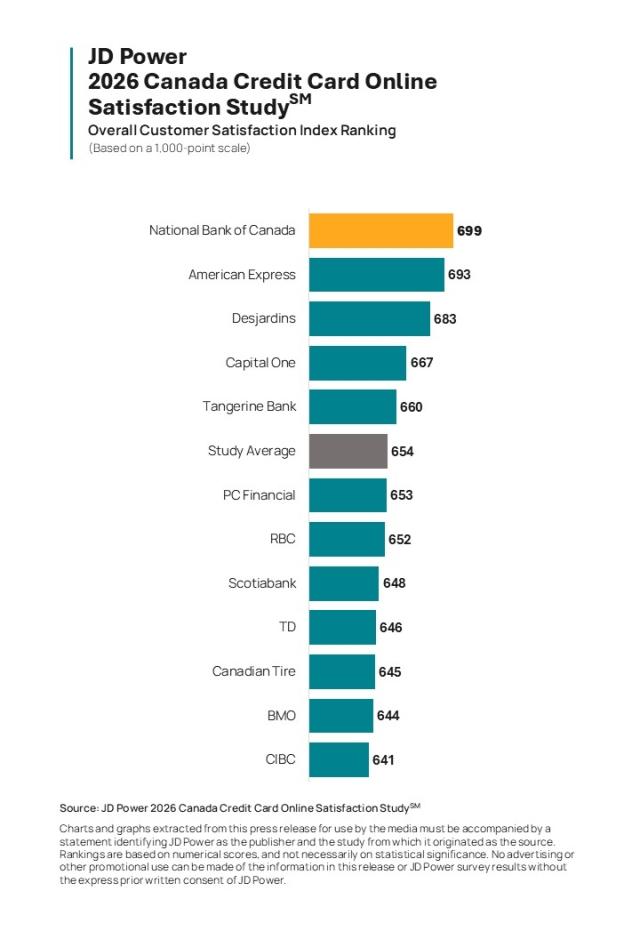

National Bank of Canada ranks highest in online credit card satisfaction with a score of 699. American Express (693) ranks second and Desjardins (683) ranks third.

The Canada Banking Mobile App Satisfaction Study; Canada Online Banking Satisfaction Study; Canada Credit Card Mobile App Satisfaction Study; and Canada Online Credit Card Satisfaction Study measure overall satisfaction with banking and credit card digital channels based on four factors(in order of importance): information; tools and capabilities; system performance; and design. The studies are based on responses from 10,167 retail bank and credit card customers and were fielded from January through March 2026.

To learn more about these studies, visit https://www.jdpower.com/business/resource/us-banking-and-us-credit-card-mobile-app-satisfaction-studies.

About JD Power

JD Power delivers mission-critical data, analytics and intelligence that help businesses improve customer experience and operational performance with confidence and clarity. Using proprietary, comprehensive data–including millions of consumer interactions and authoritative automotive datasets–combined with advanced analytics, artificial intelligence and deep industry expertise, JD Power enables leaders to respond to market shifts, make smarter decisions and drive measurable performance improvements.

As an objective source of deep insight into real-world customer interactions with brands and products, JD Power provides the independent intelligence organizations need to anticipate change, strengthen customer engagement and advance growth. Learn more at JDPower.com.

Media Relations Contacts

Gal Wilder, NATIONAL PR; 416-602-4092; [email protected]

Joe LaMuraglia, JD Power; East Coast; 714-621-6224; [email protected]

About JD Power and Advertising/Promotional Rules: www.jdpower.com/business/about-us/press-release-info

1JD Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2008). Millennials (1982-1994) ae a subset of Gen Y.