What Role is Poor Financial Literacy Playing in Financial Health of American Consumers?

Banking and Payments Intelligence Report

February 2023

What Role is Poor Financial Literacy Playing in Financial Health of American Consumers?

As U.S. bank customers start to resign themselves to another year of persistently high inflation, many have grown increasingly aware of their own lack of financial literacy.

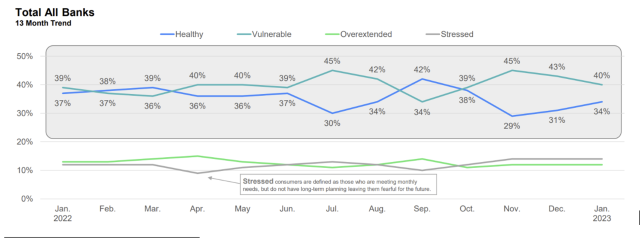

The overall financial health[1] of bank customers in America has slightly improved this month, according to JD Power data. Overall, 34% of bank customers are healthy, which is up 3 percentage points from January’s reading. That said, there is plenty of room for improvement.

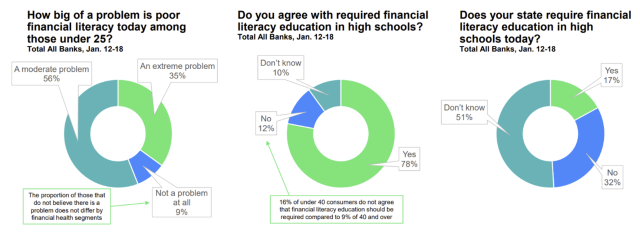

Bank customers seem to grasp that too, and they seem to have found a culprit: poor financial literacy. Virtually all (91%) bank customers say that poor financial literacy is a problem for those under age 25, and 78% believe that financial literacy should be taught in high school. Moreover, 42% of bank customers say they have significant doubts in their own levels of financial knowledge.

Overall Economic Outlook Improves Slightly

As the first quarter begins to settle in, bank customers are starting to feel slightly better about their economic situations. More than one-third (34%) of bank customers are currently classified as financial healthy, up 3 percentage points from a month ago, and 40% are vulnerable, down from 43%.

Still, despite those modest improvements, almost two-thirds (66%) of customers said that the price of goods is increasing faster than their income. While that is the lowest level of inflation recognition since the fall of 2022, the significant financial influence that inflation is having on consumers cannot be overstated.

Nearly half (45%) of customers say they have felt relief at the gas pump and another 19% are noticing grocery prices declining. Almost one-third (30%) say that they have not experienced prices declining. Unsurprisingly, that is largely concentrated in customers that are stressed or vulnerable, but even 27% of healthy customers say they have yet to feel relief.

Education is the Answer

Perhaps the most encouraging indicator this month is that bank customers seem to understand that simply waiting around for inflation to subside isn’t the only way they can navigate toward financial security. Customers want to be financially literate, and many say that has not been an easy goal to achieve. Overall, 91% believe financial literacy is at least a moderate problem today among those under age 25, with 35% viewing it as an extreme problem.

More than three-fourths (78%) believe in teaching financial literacy in high school, yet 32% say their state does not require financial literacy today, while 51% are unsure.

Banks to the Rescue

It’s clear from this latest data that many banking customers’ attitudes toward financial conditions will naturally ebb and flow. To steady customers through that natural volatility, banks can play a key role in educating their customers to be better prepared.

Our data finds that only 58% of banking customers think of themselves as financially knowledgeable, and those that are less knowledgeable are more critical of their banks. This does not only equate to lower satisfaction, customers with lower levels of understanding are less likely to open second accounts with the bank and are more likely to require customer support services. That means that banks can’t simply be passive bystanders to their customers’ financial literacy.

Banks must be proactive. That means more than just creating a library of educational articles and resources that customers will never see. Banks need to help encourage hands on learning among their customer base. They need to find better ways to encourage customers to engage with advice, then prompt them to move from it to using a tool to achieve better financial outcomes (perhaps even offering incentives to increase tool adoption), whether that is figuring out their current spending plan, directing them to check their credit score, or giving them a tool to list all their debts and prioritize which ones they are paying off first.

A better partnership between banks and their customers will only help both parties. Customers are eager for an education. Banks that give it to them will reap the benefits in the form of stronger customer loyalty and improved customer satisfaction.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in January 2023. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.