As New Technology is Integrated in Financial Services Industry, Most Bank Customers in United States Express Distrust for AI

Banking and Payments Intelligence Report

February 2024

Although the annual inflation rate is close to dipping below 3% for the first time since 2020, bank customers in the United States have yet to see major improvement in their financial situations.

According to JD Power, the percentage of U.S. bank customers that are financially healthy[1] remains near the all-time low, while new concerns are cropping up with the emergence of artificial intelligence (AI) in the financial services sector. And despite that many of these AI-driven tools could help customers, many are hesitant to trust the technology to help manage their money.

Financial Woes Continue

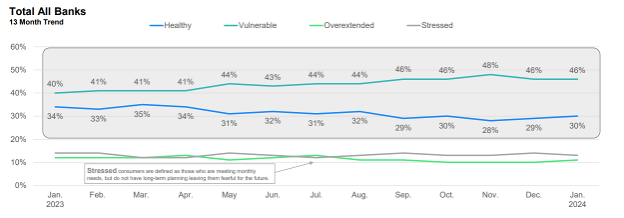

Customers’ financial health remains at a standstill. Nearly one-third (30%) of respondents are financially healthy, while 46% fall into the vulnerable category. These numbers are in line with the previous four months.

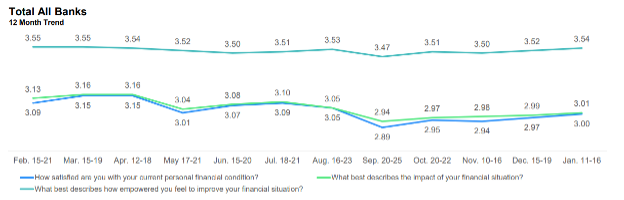

Customer sentiment regarding financial health status, stress levels and empowerment to improve one’s financial situation also remain virtually unchanged month-over-month. A small silver lining: The percentage of customers that are extremely worried that the prices for common goods will continue to rise dropped to 37% from 40% in January.

The More You Know: AI Edition

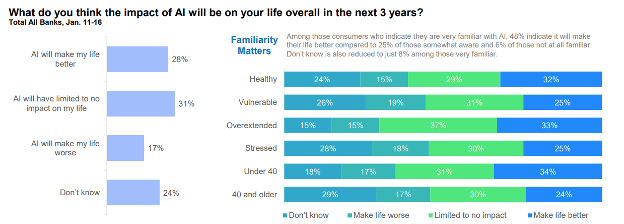

After exploding onto the scene in 2023, many industry analysts expect this to be the year when generative artificial intelligence will make a meaningful difference in consumers’ lives. Banking customers in the U.S. are skeptical. More than one-fourth (28%) believe AI (either generative or machine-learning/algorithmic) will make their lives better, while 17% think it will make their lives worse and 24% say they don’t know.

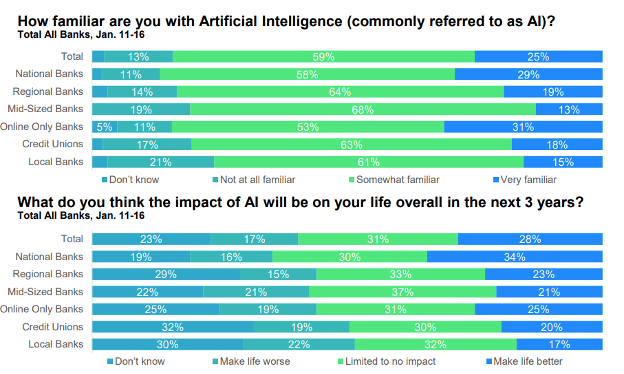

Familiarity with AI matters, as nearly half (48%) of customers that were very familiar with AI thought it would make their lives better vs. 6% of those who are not at all familiar with AI. To that point, customers of the nation’s largest banks and online-only banks are more familiar with AI than customers at credit unions or local banks.

The Hesitant Adopters

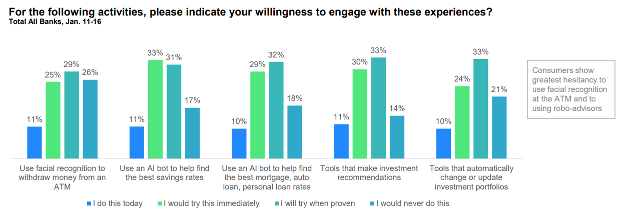

More proof of customers’ unease about AI is their willingness to let the adoption of this technology play out before they try. While many of these options are broadly available to customers, anywhere from 14% to 26% of customers (depending on the application) say they would not use AI for financial applications. Those include using facial recognition to withdraw money (26%), using tools that automatically change or update investment portfolios (21%), and using an AI bot to help find the best mortgage, auto loan or personal loan rates (18%).

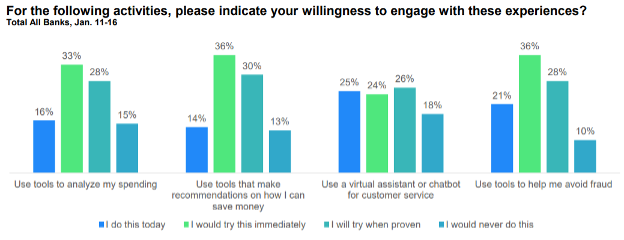

Interestingly, customers are more willing to set aside their security worries or AI fears when the tools make an immediate impact on managing their financial lives. Notably, the percentage of customers that answered they would never use AI tools was the lowest (10%) when it would them avoid fraud.

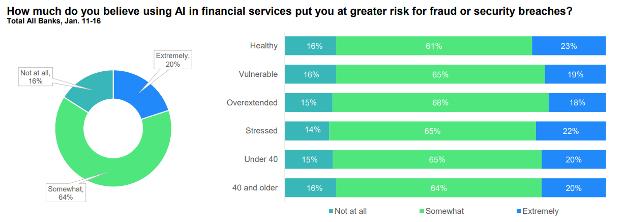

When asked how much AI in financial services put them at greater risk for fraud or security breaches, 64% of all respondents said “somewhat.” One in five (20%) thought it put them at an extreme risk, while 16% said not at all. Key to financial institutions encouraging AI driven tool adoption will be reassuring customers about tool security.

Trusting the Machines

When it comes to AI, customers seem perfectly content to let someone else be the guinea pig. But, considering the current financial landscape, they might want to be early adopters of a tool that can move money from one fund to another if AI can read or anticipate trends that might keep more of their money safe.

It’s clear that if banks are going to get customers to buy in, they need to educate them about these tools. AI can be a gamechanger for underwriting loans, managing money, and streamlining time-consuming processes, but it will all be for naught if customers don’t trust it. The banks that can boost awareness and put their customers’ minds at ease on AI stand to make major gains.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in January 2024. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]