As Mobile Wallets Gain in Popularity, Growing Number of Americans Still Prefer Convenience of Plastic

Banking and Payments Intelligence Report

January 2023

Ever find yourself away from home without your smartphone? It feels like you accidentally left an appendage behind. Modern life virtually requires that each of us has our devices accessible at any time. So how is it that most Americans still find that using a credit card is more convenient than a mobile wallet?

According to JD Power data, mobile wallet usage among Americans continues to grow in stores, but the percentage of customers that still say it is easier to use a physical credit/debit card than a mobile wallet is on the rise.

While other barriers to the widespread adoption of mobile wallets continue to erode (e.g., security concerns), customers are increasingly satisfied with the simplicity of paying with plastic, and it should inform banks and card issuers how they serve their customers in the year ahead.

Mobile Wallets Gain Acceptance

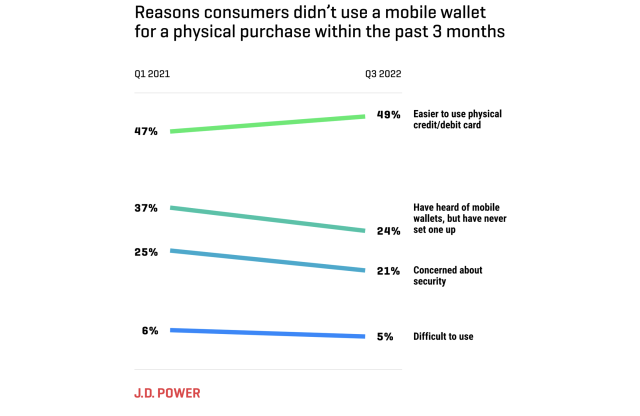

Between the first quarter of 2021 and third quarter of 2022 (the most recent quarter for which data is available), the percentage of Americans that said that they used a mobile wallet at some point in the previous three months increased to 49% from 38%. That increase reflects a significant erosion of some historical barriers to adoption.

Chief among them: trial. The percentage of people who said they have heard of mobile wallets, but have never set one up, declined to 24% from 37%, and those that said that are concerned about security declined to 21% from 25%. A small decline—5% from 6%—was seen in the percentage of customers who found mobile wallets difficult to use.

Plastic Still Makes It Possible

Usability continues to be an issue holding back wide-spread adoption of mobile wallets. The percentage of customers who said they do not use mobile wallets because it is less convenient than a card actually increased to 49% from 47% in 2022. One potential reason for this rise? The emergence of contactless cards.

In October 2022, Visa reported on its quarterly earnings call that contactless card had accounted for 28% of its U.S. transactions, up from 20% in January 2022. This is welcome news to issuers who lose brand recognition and pay extra (in the case of Apple Pay transactions) at the point of sale when customers pay with a wallet instead of a card.

The Behavioral Opportunity

The growth in contactless issuance has breathed new life into cards and it bodes well for continued physical card preference at the point of sale. Changing customer behavior is one of the hardest goals for a company to realize, and much to the chagrin of some mobile wallet providers, the ubiquity of smartphone use hasn’t quite translated into automatic adoption of mobile wallets, yet.

As 2023 begins, and Americans contend with a challenging economic environment, this data should inform how issuers should tailor their customer acquisition and existing customer engagement efforts. While mobile certainly holds some allure, contactless cards can keep the tech giants’ efforts to co-opt the American payment landscape at bay. As for how long that will be the case, time – and how issuers seize this opportunity – will tell.

Find out More

This Banking and Payments Intelligence Report is based on responses from 3,588 retail bank customers nationwide and was fielded in Q1 2021 and Q3 2022. It was authored by Paul McAdam, senior director of banking and payments intelligence, and John Cabell, managing director of payments intelligence, at JD Power. Please contact us at the numbers below to connect with Mr. Cabell or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]