JD Power Revises EV Retail Share Forecast

Despite Overall Rise in EV Sales Volume, Consumer Interest and Adoption Slower Than Expected in First Half of 2024

E-Vision Intelligence Report

August 2024

Key Findings

- Near-Term EV Forecast Revised Down: JD Power has revised down its 2024 and 2025 EV market share forecast, projecting 9% total EV market share in 2024, which translates to approximately 1.2 million in sales of battery electric vehicles (BEVs), excluding plug-in hybrids (PHEVs) and hybrids (HEVs). The 2024 EV forecast was revised down from 12%. Longer term, JD Power projects annual EV sales volumes will reach 36% market share by 2030 and 58% market share by 2035.

- Growth of PHEVs, Lingering Concerns About Public Charging Create Hurdles to Adoption: While 60 different EV models are now available, the number of PHEV options has also grown considerably, reaching 45 models and accounting for 1.8% of total sales. The growth of PHEVs has created additional substitutes for gas-powered vehicles and increased competition for EVs. The other persistent headwind on EV sales has been consumer concern with public charging infrastructure.

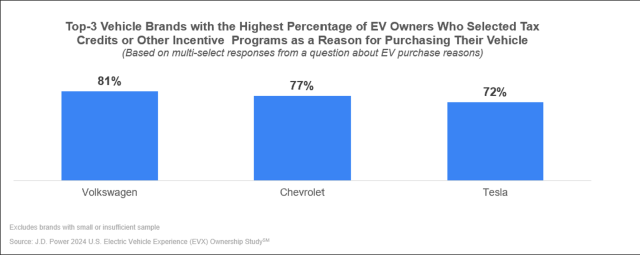

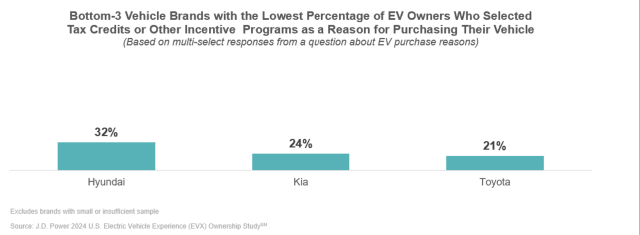

- Incentives, New Models and Returning Lessees Could Spark More Growth: EV affordability and availability scores have been improving for two consecutive months, with current tax incentives and lease deals making EVs more affordable than their gas-powered counterparts, in many categories. Continued improvements in overall accessibility of EVs and increased volume from returning EV lessees—94% of whom say they are likely to consider another BEV—are likely to drive a surge in EV sales volume during the next two years.

Executive Summary

Welcome to the messy middle of the EV evolution. As manufacturers continue to refine their go-to-market EV strategies, offering an increasingly varied mix of powertrains ranging from HEVs to PHEVs to BEVs, the adoption curve continues to grow but in a less predictable, more volatile fashion. Overall, BEV sales are up 35,000 units through July 2024, and while that is a clear sign of continued momentum, it is a slower growth rate than previously expected. In this report, we’ll discuss how this trend has affected our EV sales forecast and dive into the data to better understand the dynamics at play in the current market.

This E-Vision Intelligence Report dives into key data points trending in each monthly EV Index update, along with other data points gathered from JD Power studies and pulse surveys, to spotlight emerging trends and important shifts in EV consumer sentiment.

EV Market Share Forecast Revised Down

Based on the current mix of EV interest, availability, adoption, affordability, infrastructure and customer experience metrics tracked each month at JD Power, we are projecting total EV market share will reach 9%, or 1.2 million units, by the end of this year. That forecast is revised down from 12% in January 2024, based on a slower-than-expected growth rate for the first half of the year.

Longer term, we are projecting EV sales will reach 36% of the total U.S. retail market by 2030 and 58% by 2035. The current rate of slower-than-expected sales volume is being driven by a combination of relatively near-term variables that will fade as EV adoption continues to reach critical mass.

Consumers Confront Mixed Signals

One major driver of the slower-than-expected EV growth rate in the first half of this year has been increased competition in the market for gasoline-powered vehicle alternatives. While HEVs and BEVs currently account for the lion’s share of sales in this category at 8.6% and 8.4%, respectively, PHEVs have recently gained more widespread attention and now account for 1.8% of retail sales. That’s up from just 0.6% in 2020 across 45 different models that are now available. However, while PHEV sales have been increasing recently, JD Power customer satisfaction data suggests this surge in interest may be temporary. PHEVs score significantly lower than BEVs in nine of the 10 categories tracked in the JD Power 2024 U.S. Electric Vehicle Experience Ownership Study, particularly when it comes to battery range and total cost of ownership.

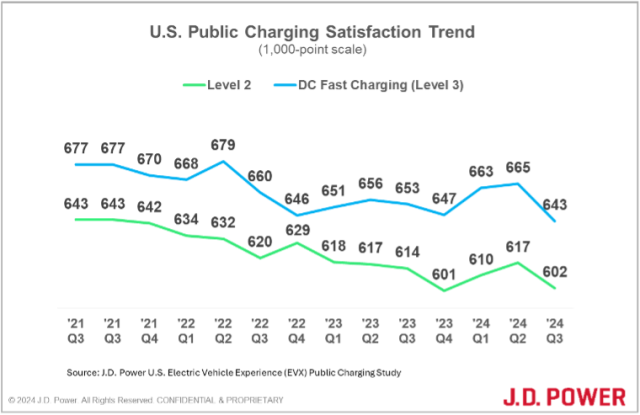

The other headwind on EV sales has been ongoing consumer concerns with public charging infrastructure. According to the JD Power 2024 U.S. Electric Vehicle Experience (EVX) Public Charging Study,SM the ease of home charging is the most satisfying single aspect of the EV ownership experience and public charging availability is the least-satisfying aspect. However, customer satisfaction with both Level 2 and DC Fast Charging segments has improved for two consecutive quarters—a first for the study which is in its fourth year. As public charging infrastructure continues to improve, this headwind to EV adoption should dissipate.

Expect an EV Inflection Point

EV availability and affordability metrics have continued to improve for the past two months as a surge in new mainstream models rolls out nationwide. Currently, 66% of new-vehicle buyers have a viable EV alternative available to them and, in many cases, EVs are now less expensive to own than their gas-powered counterparts.

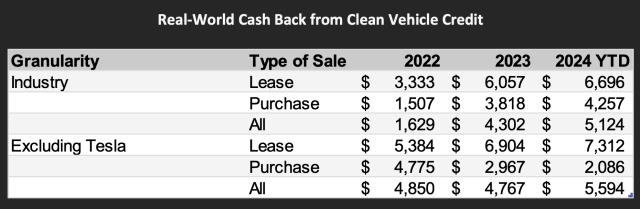

One important detail in current EV sales volumes is the extraordinarily high proportion of leasing activity. Due to tax incentives introduced under the Inflation Reduction Act, which allow the $7,500 Clean Vehicle Credit to pass through on leased EVs, 86% of premium BEV transactions (excluding Tesla) are leases. Similarly, 72% of mass market BEV transactions are leases. Conversely, only 11% of Tesla transactions are leases. When these leasing customers return to market, we expect a significant surge in new EV volumes, especially from traditional franchise dealers. Currently, 94% of current BEV owners say they are likely to consider another BEV for their next vehicle, according to JD Power data.

Methodology

This JD Power E-Vision Intelligence Report is based on data and insights from the JD Power EV Index, the JD Power EV Retail Share Forecast, the JD Power 2024 U.S. Electric Vehicle Experience (EVX) Ownership Study,SM the JD Power 2023 U.S. Electric Vehicle Experience (EVX) Public Charging StudySM and the JD Power U.S. Electric Vehicle Consideration (EVC) Study.SM The JD Power EV Index is an analytics tool to benchmark the growing EV market in the United States. It tracks millions of data points aggregated into six categories—interest, availability, adoption, affordability, infrastructure and experience—to evaluate the progress to parity of EVs with gas-powered vehicles in the U.S. Each month, the JD Power electric vehicle practice will analyze these data points, and others to spotlight emerging trends and important shifts in consumer sentiment that are helping to define the fast-moving EV marketplace.

Find out More

This report was authored by Elizabeth Krear, vice president, electric vehicle practice; Brent Gruber, executive director, electric vehicle practice; Stewart Stropp, executive director, electric vehicle practice; and Kristen Richter, senior manager, electric vehicle practice. The JD Power E-Vision initiative is a company-wide program focused on maximizing JD Power industry-leading EV data, analytics, insights and solutions. Please contact us at the numbers below to connect with the authors or to learn more about the underlying research.

Media Contacts

Shane Smith; East Coast; 424-903-3665; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]