EV Incentives to Wield Heavy Hand in Q4 2023 and Q1 2024 Sales Volumes

E-Vision Intelligence Report

October 2023

EV Incentives to Wield Heavy Hand in Q4 2023 and Q1 2024 Sales Volumes

Key Findings

- 7,500 Reasons to Wait Until January to Buy an EV: Starting in January 2024 buyers eligible for the $7,500 Clean Vehicle Credit will be able to transfer those funds to the dealer for use as a down payment at the point of sale. This is a significant departure from the current implementation of the credit, whereby eligible buyers do not receive the credit until they receive their tax returns. Whether this new treatment of the credit will cause active EV shoppers to wait until January or buy in the fourth quarter will hinge largely on how well dealers and original equipment manufacturers (OEMs) handle end-of-year incentives and customer education.

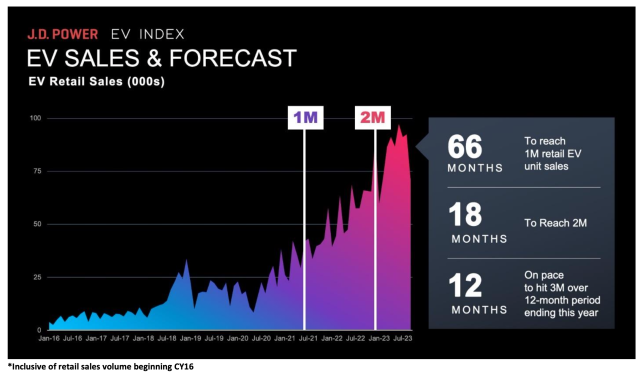

- EV Sales on Pace to Hit Three Million by Year End, Four Million by End of Q3 2024: The long-term trend in EV market share has grown significantly from 2.6% of all new-vehicle sales in February 2020 to 9% in September 2023, putting total EV sales volume on pace to reach the three-million-unit milestone by December of this year. At this pace, JD Power projects EV sales to top four million units by the end of Q3 2024.

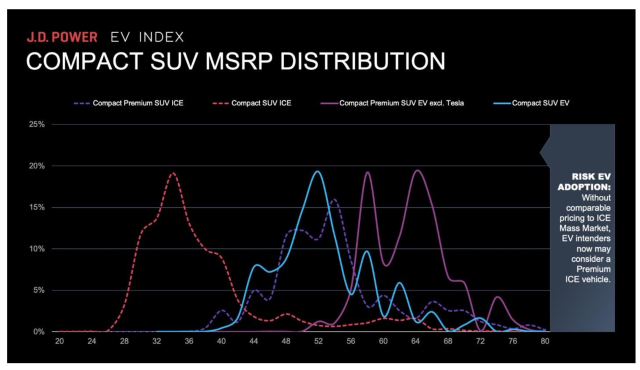

- New Calculus of Cross-Shopping Emerges in Compact SUV Market: Despite overall improvements in EV affordability, a stark discrepancy still exists between EV and internal combustion engine (ICE) vehicle pricing in the compact SUV segment, which is the highest volume retail sales segment in the United States. The dislocation has introduced a new cross-shopping phenomenon for the 67% of prospective EV buyers who are also considering non-EVs, whereby for the same price as a mass market EV, they could purchase a luxury ICE vehicle of the same size.

Executive Summary

“What do I have to do to put you in a new EV today?” That’s a question more automobile dealers will be asking in the fourth quarter of 2023 as a complex mix of growing consumer interest, new vehicle incentives and a dislocation of conventional pricing dynamics has new-vehicle shoppers scratching their heads and looking for guidance.

According to JD Power, with total EV market share now hitting the 9% mark and total EV sales on track to hit three million by the end of this year, the stage is set for rapid-fire growth. Exactly when those sales will happen—and which OEMs and dealers will be the biggest beneficiaries of the transformation—will come down to strategic use of incentives and a concerted effort to educate consumers on the intricacies of EV pricing.

This E-Vision Intelligence Report dives into key data points trending in each monthly EV Index update, along with other data points gathered from JD Power studies and pulse surveys, to spotlight emerging trends and important shifts in EV consumer sentiment.

Incentives Loom Large

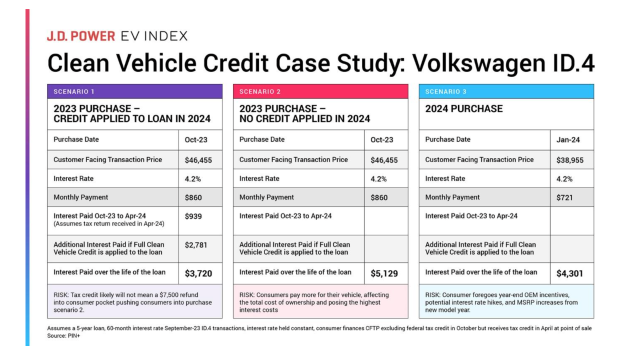

A big change to the Clean Vehicle Credit is coming in January 2024. The U.S. Department of Treasury introduced a new rule this month that will make it possible for eligible consumers to transfer the $7,500 tax credit to the dealer for use as a down payment at the point of sale. While the criteria for qualifying for the credit is still fairly complicated, and requires knowing things about the location where the vehicle was assembled and details on the sourcing of critical minerals used in the construction of vehicle batteries that most mainstream consumers do not know, the execution of the credit itself will become much easier. Prior to 2024, eligible buyers would not receive the credit until they receive their tax returns.

The chart below illustrates the differences in real-world dollar terms in how the 2023 application of the Clean Vehicle Credit differs from the 2024 application of the credit using a Volkswagen ID.4 as an example. In 2023, a buyer would pay $139 more per month for a loan and, depending upon whether they purchased the vehicle prior to receiving their tax returns for the year, they could end up paying upwards of $828 more in interest during the life of their auto loan than buyers who wait for January 2024 to purchase the same vehicle.

All of these details introduce a level of consumer education that dealers and OEMs have never had to contend with before. In addition to the new filing and administrative details dealership finance and insurance (F&I) departments will face when applying the credit to a downpayment in 2024, the dealership will also need to make sure customers understand how these incentives will affect their bottom-line costs. Whether this new structure will cause active shoppers to hold off on new purchases until January, or whether they will purchase now may come down to what kinds of additional incentives dealers and OEMs offer in the holiday sales push in the final two months of the year and how well they explain the details to prospective buyers.

EV Sales Reaching Critical Mass

Regardless of whether the new incentive structures will spur sales before or after the New Year, it is clear that momentum is building in total EV sales volume. According to the JD Power EV Index, it took five and a half years (66 months) for total EV retail sales to hit one million sales. From there, it took only 18 months to reach two million. Based on the latest JD Power forecast, retail EV sales will hit three million during the 12-month period ending in December of this year and four million by end of Q3 2024.

More for Your Money?

One complicating factor that could be a drag on near-term EV sales, however, is the pricing imbalance that currently exists between EVs and ICE vehicles in the booming compact SUV segment. Currently, the bulk of mass market compact EV SUV sales are pricing at around $52,000. That compares with just $34,000 for comparable mass market ICE SUVs. Meanwhile, ICE vehicles in the compact premium SUV segment are trading at around $53,000, vs. EVs in the compact premium SUV segment selling for $60,000 or more.

This has created a dislocation where price-sensitive shoppers in the compact SUV market could likely be cross-shopping a mass market EV against a premium ICE vehicle. Based on the latest JD Power 2023 U.S. Electric Vehicle Consideration (EVC) Study, 67% of new-vehicle shoppers who are currently considering an EV are also considering non-EVs. Until the pricing differential between mass market and luxury EV and ICE vehicles is more balanced, many of these buyers may be swayed to choose ICE.

Methodology

This JD Power E-Vision Intelligence Report is based on data and insights from the JD Power EV Index, the JD Power EV Retail Share Forecast and the JD Power U.S. Electric Vehicle Consideration (EVC) Study. The JD Power EV Index is an analytics tool to benchmark the growing EV market in the United States. It tracks millions of data points aggregated into six categories—interest, availability, adoption, affordability, infrastructure and experience—to evaluate the progress to parity of EVs with ICE vehicles in the U.S. Each month, the JD Power electric vehicle practice will analyze these data points, and others to spotlight emerging trends and important shifts in consumer sentiment that are helping to define the fast-moving EV marketplace.

Find out More

This report was authored by Elizabeth Krear, vice president, electric vehicle practice; Brent Gruber, executive director, electric vehicle practice; Stewart Stropp, executive director, electric vehicle practice; and Kristen Richter, senior manager, electric vehicle practice. The JD Power E-Vision initiative is a company-wide program focused on maximizing JD Power industry-leading EV data, analytics, insights and solutions. Please contact us at the numbers below to connect with the authors or to learn more about the underlying research.

Media Contacts

Shane Smith; East Coast; 424-903-3665; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]