It’s a Buyer’s Market for EVs. Where are the Buyers?

E-Vision Intelligence Report

June 2024

Key Findings

- EVs More Widely Available and Affordable Than Ever: The majority of premium (70.1%) and mainstream (55.7%) vehicle buyers now have a suitable electric vehicle (EV) option available in the marketplace and the prices for these vehicles has never been lower. The average total cost of ownership (TCO) for a premium EV fell to $62,600 in May and the average TCO for a mainstream EV is now $58,100. In many cases, EVs are now more affordable than their gasoline-powered counterparts.

- EV Consideration and Adoption Stalled: Overall, 59.5% of new-vehicle shoppers say they are either “very likely” or “somewhat likely” to consider buying an EV in the next 12 months, a slight increase from April (58.2%), but down from the highest levels observed in the fourth quarter of 2023. Real-world EV adoption rates have been flat at 8.4% since March 2024.

- Next Several Months Pose Critical Test for Mainstream Consumer Demand: Two major impediments to widespread mass market EV adoption have been a significant price premium vs. comparable gas-powered vehicles and a notable lack of vehicle options in the mainstream market. During the past two months, both of those trends have shifted sharply, with major mainstream launches and trim expansions planned during the next several quarters. Consumer response to these changing market dynamics during the next several months will be a key indicator of future EV demand.

Executive Summary

It’s become impossible to ignore the rising tide of negative sentiment about consumer demand for EVs. But when we look deep into the data on EV market dynamics, consumer sentiment and infrastructure development, we find that it is still too early to say exactly how shoppers will respond to major new improvements in EV affordability and availability. The next several months will be critical in shaping that longer-term forecast.

This E-Vision Intelligence Report dives into key data points trending in each monthly EV Index update, along with other data points gathered from JD Power studies and pulse surveys, to spotlight emerging trends and important shifts in EV consumer sentiment.

EV Availability and Affordability Surges

The EV market has skewed premium since its inception, and that is still the case. Tesla, a premium brand, accounted for 50% of all EVs sold in the U.S. in May, and 70.1% of premium vehicle buyers currently have a comparable EV option available. In addition, many premium EVs are now more affordable than comparable gas-powered vehicles. But that dynamic is starting to shift into the mass market, as well. In fact, mainstream EV availability has surged considerably since March 2024, with 55.7% of mainstream buyers now having a viable EV option. A combination of manufacturer incentives and growth of lower-priced trims in existing EV models is driving this surge. Additionally, new mainstream models in the popular crossover SUV segment are coming to market, meeting more consumers’ needs, including the Honda Prologue and Chevrolet Equinox EV.

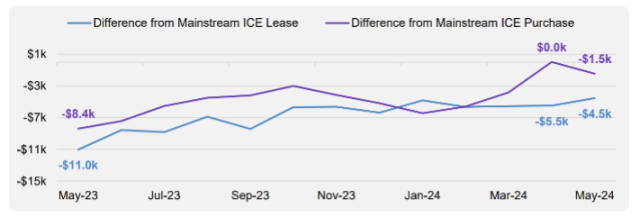

When it comes to affordability, mainstream EVs are now just $1,500 more expensive, on average, than their gas-powered counterparts. That gap has shrunk from a high of $8,400 in May 2023. When looking at specific models, in many cases, EVs have become considerably cheaper than gas-powered vehicles. The Ford F-150 Lightning, for example, now has an average customer-facing transaction price (CFTP) of $53,494 after federal tax credits, which is $5,073 cheaper than the average CFTP of a gas-powered F-150.

Mainstream Affordability

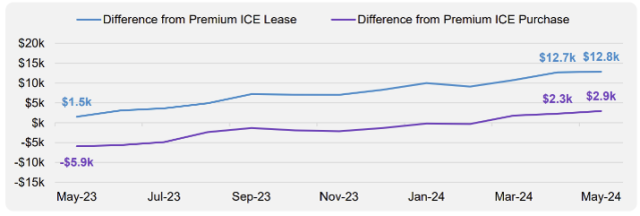

Premium Affordability

Demand Stalls

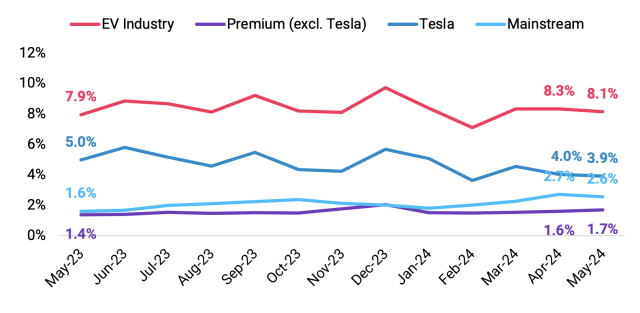

Despite these recent improvements in affordability and availability, total EV industry market share has been largely flat for the past three months, currently accounting for 8.4% of total vehicle sales. When it comes to consumer sentiment, 59.5% of new-vehicle shoppers say they are either “very likely” or “somewhat likely” to consider buying an EV in the next 12 months, a slight increase from April (58.2%), but down from the highest levels observed in the fourth quarter of 2023.

Digging deeper into those numbers, we find that the month-over-month increase in EV consideration is being driven by vehicle shoppers who say they are “very likely” to consider an EV. Conversely, the percentage of vehicle shoppers who say they are “very unlikely” to consider an EV is trending down.

EV Retail Share

Mainstream EV Adoption: Still in the Early Days

While it is tempting to read these data points as an indication of waning consumer interest in EVs, it is important to keep perspective of the larger context of the transformation currently unfolding in the automobile industry. The industry is at a tipping point in the evolution of the EV market, whereby the initial influx of premium vehicles that appealed largely to early adopters is now giving way to more mainstream models designed—and priced—for a mass-market audience. Importantly, this is only the third consecutive month that we’re seeing an improving trend toward mainstream affordability and availability.

The next several months will be critical to watch as mainstream EV models are being offered at steep discounts when compared with comparable gas-powered models. Once the barriers of cost and availability are no longer a factor in the EV purchase equation for consumers, the focus will shift squarely to driving and charging experience as the true gauges of consumer sentiment in the EV market.

Methodology

This JD Power E-Vision Intelligence Report is based on data and insights from the JD Power EV Index, the JD Power EV Retail Share Forecast, the JD Power 2024 U.S. Electric Vehicle Experience (EVX) Ownership Study, the JD Power 2023 U.S. Electric Vehicle Experience (EVX) Public Charging Study and the JD Power U.S. Electric Vehicle Consideration (EVC) Study. The JD Power EV Index is an analytics tool to benchmark the growing EV market in the United States. It tracks millions of data points aggregated into six categories—interest, availability, adoption, affordability, infrastructure and experience—to evaluate the progress to parity of EVs with gas-powered vehicles in the U.S. Each month, the JD Power electric vehicle practice will analyze these data points, and others to spotlight emerging trends and important shifts in consumer sentiment that are helping to define the fast-moving EV marketplace.

Find out More

This report was authored by Elizabeth Krear, vice president, electric vehicle practice; Brent Gruber, executive director, electric vehicle practice; Stewart Stropp, executive director, electric vehicle practice; and Kristen Richter, senior manager, electric vehicle practice. The JD Power E-Vision initiative is a company-wide program focused on maximizing JD Power industry-leading EV data, analytics, insights and solutions. Please contact us at the numbers below to connect with the authors or to learn more about the underlying research.

Media Contacts

Shane Smith; East Coast; 424-903-3665; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]