COSTA MESA, Calif.: 26 April 2018 — Retail bank investments in technology are paying off in the form of substantial numbers of digital-only bank customers, but some of that growth may be coming at the expense of customer satisfaction. According to the JD Power 2018 U.S. Retail Banking Satisfaction Study,SM 28% of retail bank customers are now digital-only, but they are the least satisfied among all customer segments examined in the study.

“There is no doubt that digital banking channels give banks an enormous opportunity to reduce costs, but the risk is that those cost savings come with lower levels of customer engagement,” said Paul McAdam, Senior Director of the Banking Practice at JD Power. “Right now, retail banks need to address the growing digital divide that is emerging within customer segments. Successfully navigating that transition will require banks to provide better, more personalized advice that is consistent across both digital and branch interactions and to ensure that customer needs are met, regardless of channel.”

Following are some key findings of the study:

- Digital-only and branch-only customers are least-satisfied customer segments: Overall satisfaction is lowest among retail bank customers who exclusively used online or mobile banking channels during the past three months (791 on a 1,000-point scale). Customers who exclusively used a branch are slightly more satisfied (804). The segment with the highest level of overall satisfaction—823—is branch-dependent digital customers, the group that used the branch two or more times in the past three months and also used online or mobile banking. This group is followed by digital-centric branch-using customers (808), who used the branch once in the past three months and used online or mobile banking.

- Communication is where relationships fall short: The lower satisfaction scores found among digital-only customers are largely driven by weaker performance across three factors in the study: communication and advice; products and fees; and new account opening.

- Digital divide largest among Millennial[1] and Gen X bank customers: The gap in satisfaction between digital-centric and branch-dependent customers cuts across all generations of retail bank customers, but it is most pronounced among Millennials (35-point satisfaction gap) and Gen X (24-point satisfaction gap), bucking the conventional wisdom that younger banking customers do not like to use branches.

- Big banks lead the way on digital transformation: Big banks have the largest concentration of digital-centric customers (47%). Within the big and regional bank segments, Capital One and Bank of America have the highest percentages of digital-centric customers (55% and 53%, respectively), giving them a significant lead in digital transformation.

“While the retail banking industry has a great deal of work to do to bridge the growing digital divide, some leaders have already begun to make huge progress on the digital learning curve,” McAdam said. “Some of the best practices being pioneered today by digital leaders include highly personalized digital interactions along with branch transformation efforts that serve the needs of both digital-centric and branch-dependent customers.”

Study Rankings

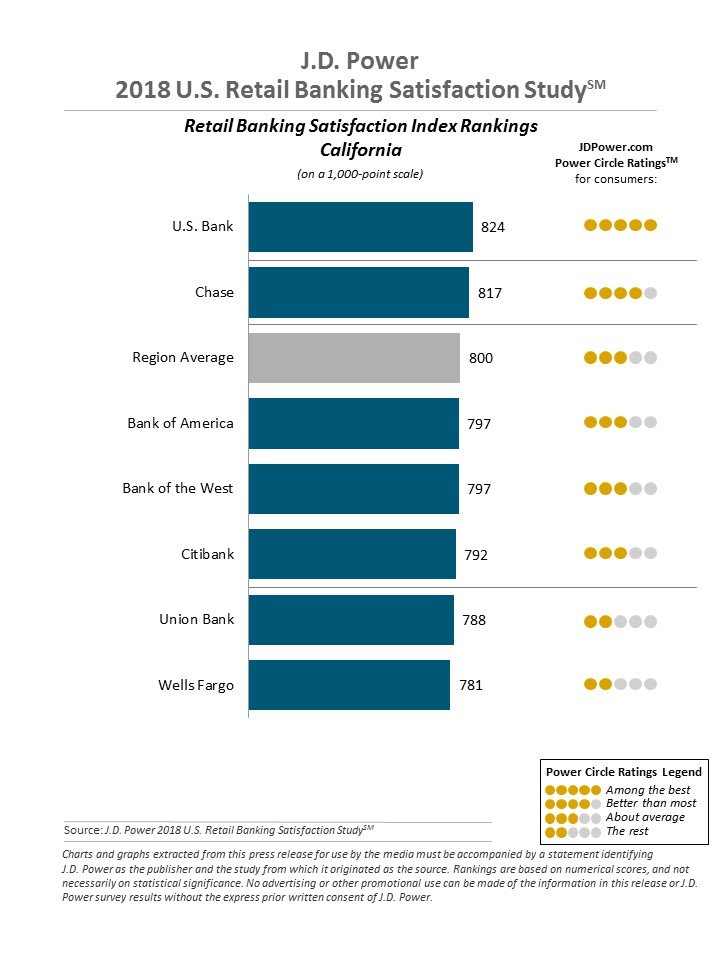

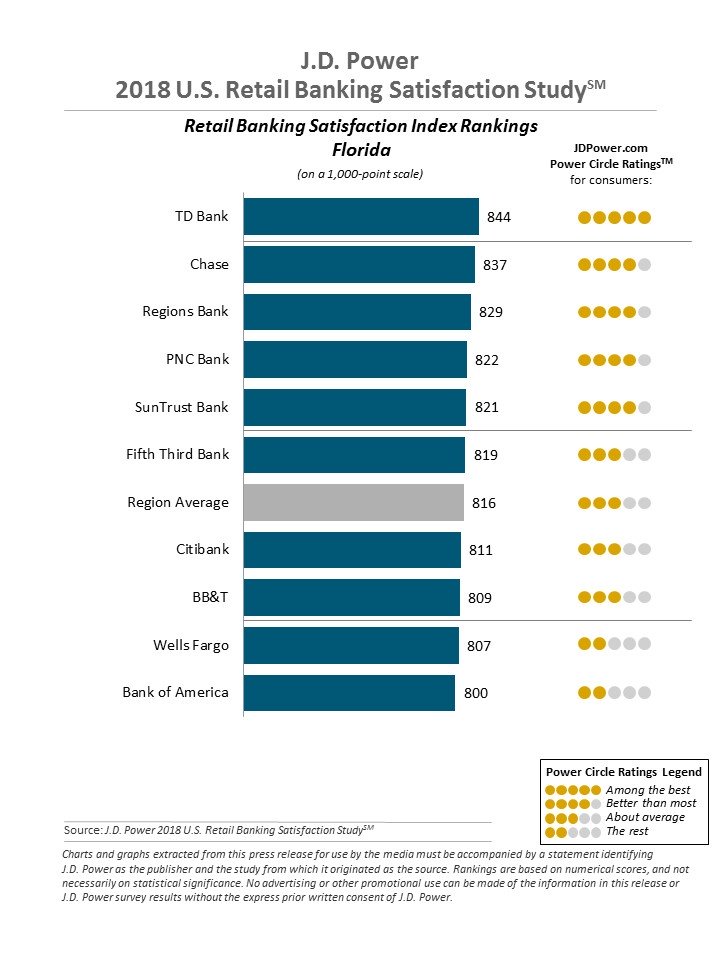

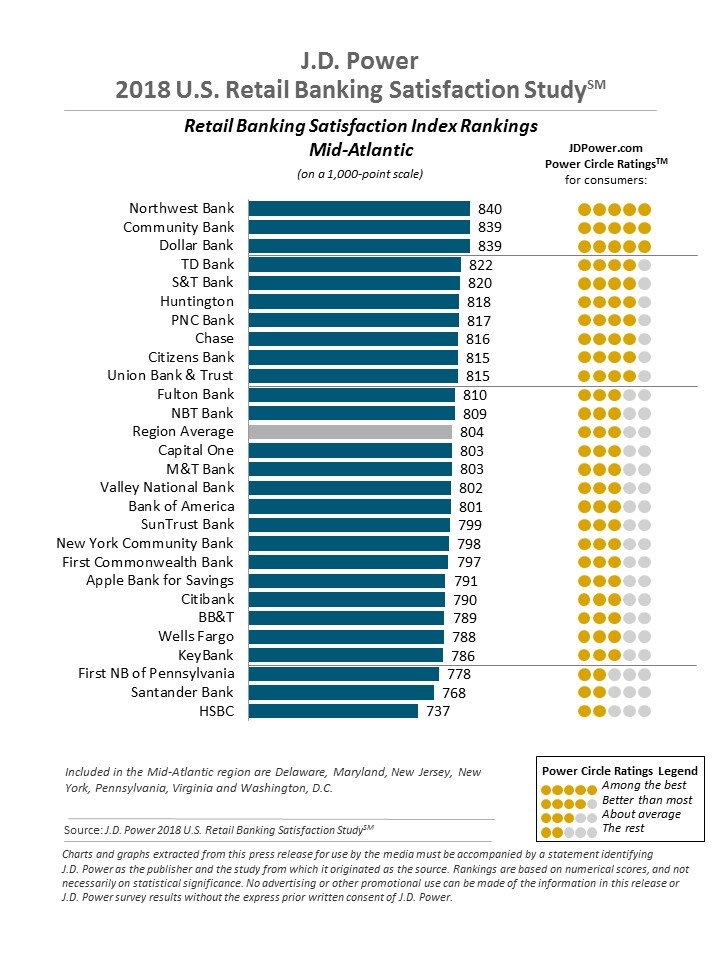

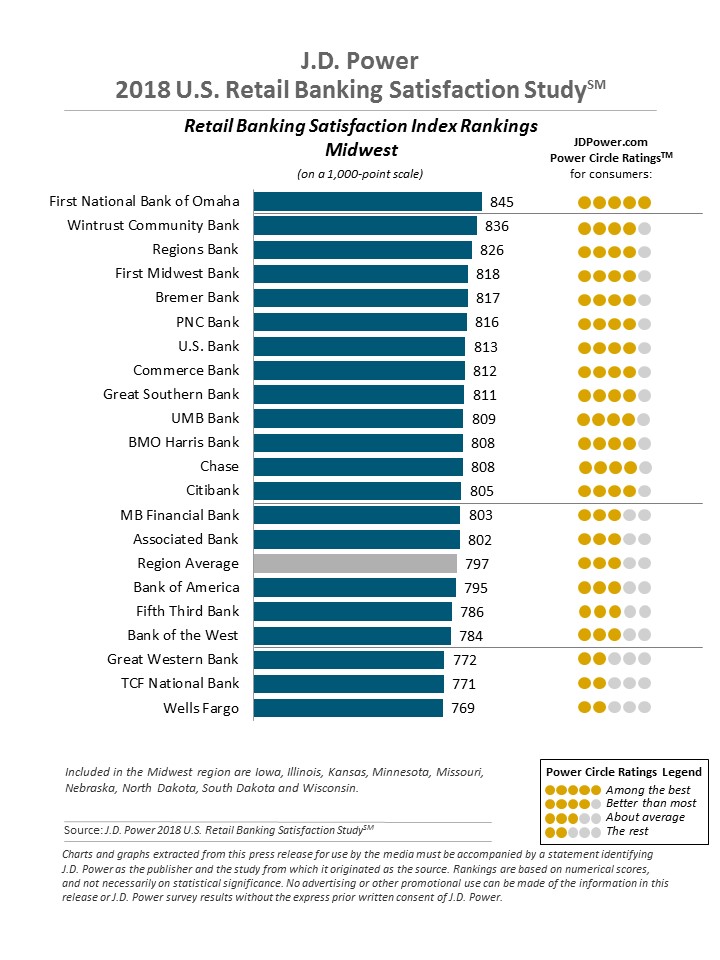

The study measures customer satisfaction with banks in 11 regions of the United States. The scores reflect satisfaction of the entire retail banking customer bases of these banks, representing a broader group of customers than just the branch-dependent and digital-centric segments. The JD Power award recipients with the highest retail banking customer satisfaction scores by region are:

California Region: U.S. Bank (824)

Florida Region: TD Bank (844)

Mid-Atlantic Region: Northwest Bank (840)

Midwest Region: First National Bank of Omaha (845)

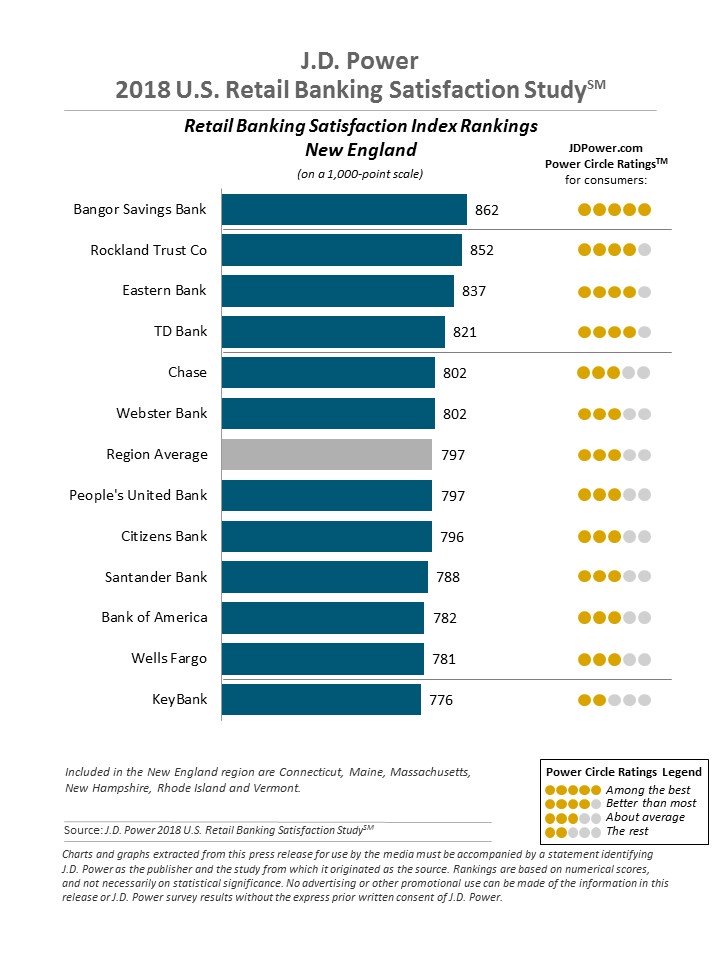

New England Region: Bangor Savings Bank (862)

North Central Region: City National Bank (W.V.) (854)

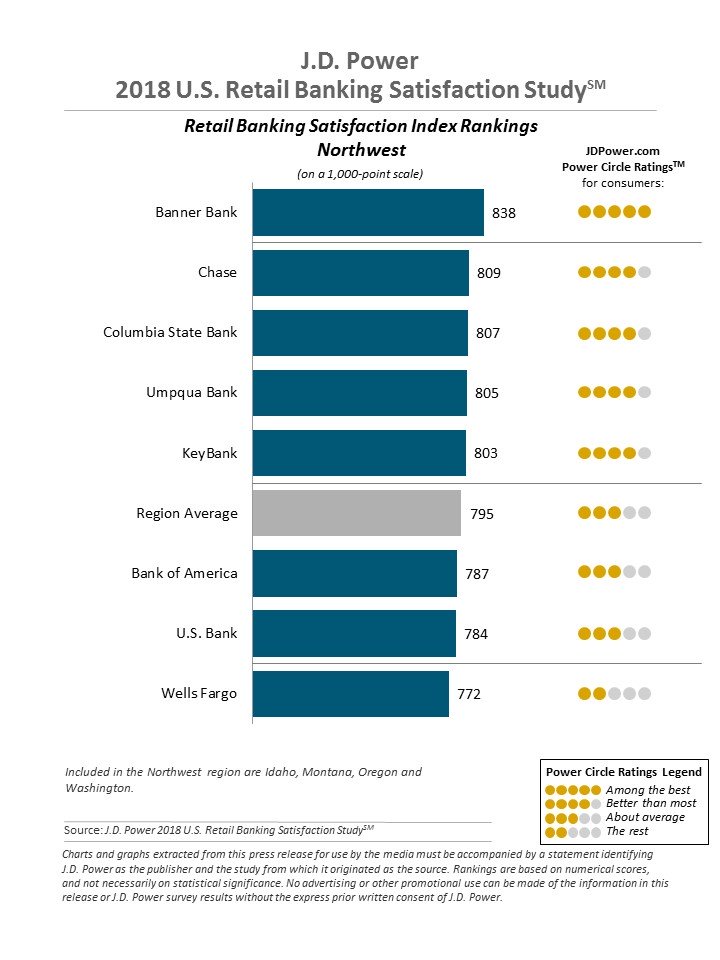

Northwest Region: Banner Bank (838)

South Central Region: Trustmark National Bank (856)

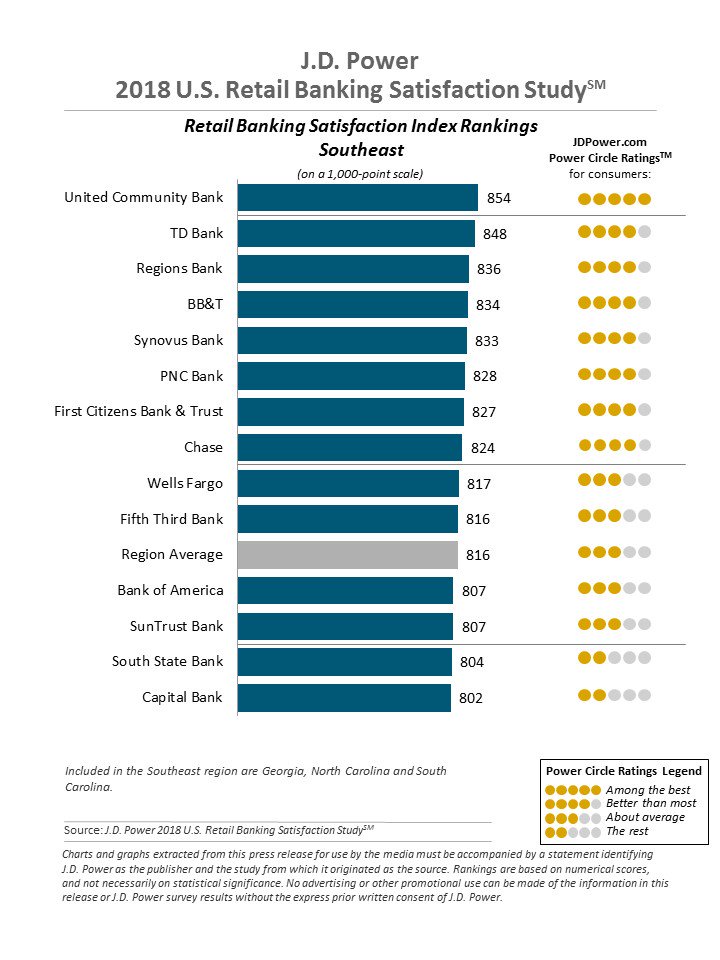

Southeast Region: United Community Bank (854)

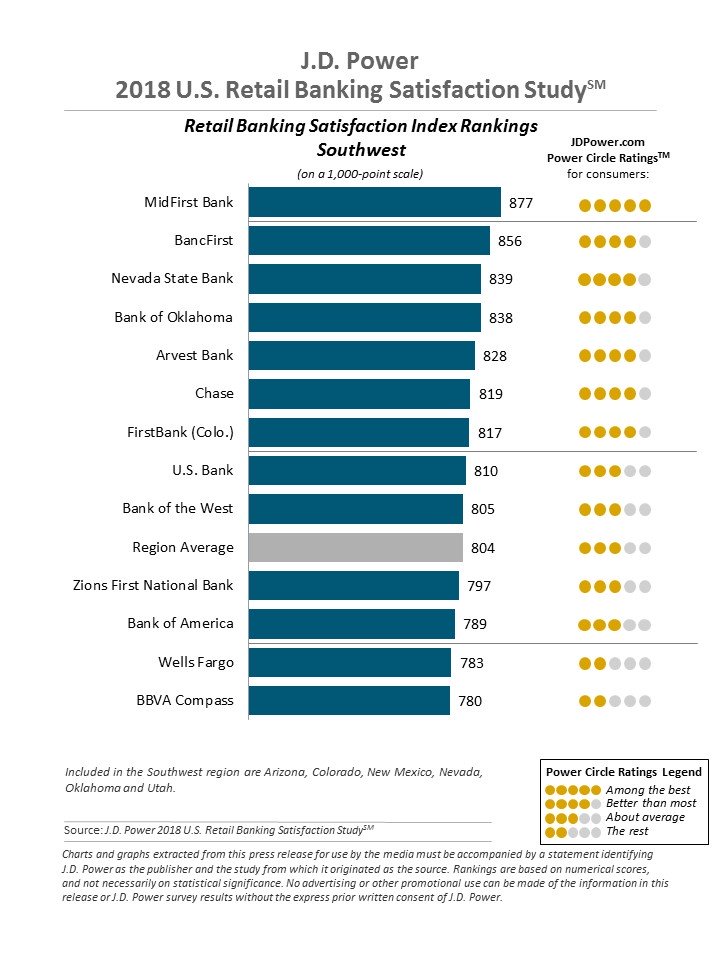

Southwest Region: MidFirst Bank (877)

Texas Region: Frost Bank (873)

The 13th annual U.S. Retail Banking Satisfaction Study measures satisfaction in six factors (listed in alphabetical order): channel activities; communication and advice; convenience; new account opening; problem resolution; and products and fees. Channel activities include seven subfactors (listed in alphabetical order): assisted online service; ATM; branch service; call center service; IVR/automated phone service; mobile banking; and online banking.

The study is based on responses from more than 88,000 retail banking customers of 200 of the largest banks in the United States regarding their experiences with their retail bank. It was fielded in quarterly waves from April 2017 to February 2018.

For more information about the U.S. Retail Banking Satisfaction Study, visit http://www.jdpower.com/business/resource/us-retail-banking-satisfaction-study.

JD Power is a global leader in consumer insights, advisory services and data and analytics. These capabilities enable JD Power to help its clients drive customer satisfaction, growth and profitability. Established in 1968, JD Power is headquartered in Costa Mesa, Calif., and has offices serving North/South America, Asia Pacific and Europe. JD Power is a portfolio company of XIO Group, a global alternative investments and private equity firm headquartered in London, and is led by its four founders: Athene Li, Joseph Pacini, Murphy Qiao and Carsten Geyer.

Media Relations Contacts

Geno Effler; Costa Mesa, Calif.; 714-621-6224; [email protected]

John Roderick; St. James, N.Y.; 631-584-2200; [email protected]

About JD Power and Advertising/Promotional Rules www.jdpower.com/business/about-us/press-release-info

[1] JD Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); and Gen Y (1977-1994). Xennials (1978-1981) and Millennials (1982-1994) are subsets of Gen Y.