Direct Banks Setting Benchmark for Customer Satisfaction, JD Power Finds

Capital One 360 Ranks Highest in Overall Satisfaction among Branchless Banks

COSTA MESA, Calif.: 28 June 2018 — Direct banks continue to outperform traditional retail banks in overall customer satisfaction, but these branchless institutions are showing some signs of vulnerability. According to the JD Power 2018 U.S. Direct Banking Satisfaction Study,SM direct banks have lost ground to traditional retail banks in terms of customer understanding and mobile experience. Key performance metrics—providing tailored information to meet customer needs, understanding product features and understanding fee structures—have declined year over year.

“Direct banks have traditionally occupied a niche of the retail banking marketplace where they serve mainly as secondary banks with competitive products and strong digital- and phone-based tools that drive high levels of customer satisfaction,” said Bob Neuhaus, Financial Services Consultant at JD Power. “However, these banks still represent less than 10% of industry deposit share and they are experiencing some deterioration in customer satisfaction with customer understanding and mobile offerings. If they want to evolve from a secondary to a primary bank relationship, they need to focus on cross-channel consistency and ramp up their digital capabilities.”

Following are some key findings of the 2018 study:

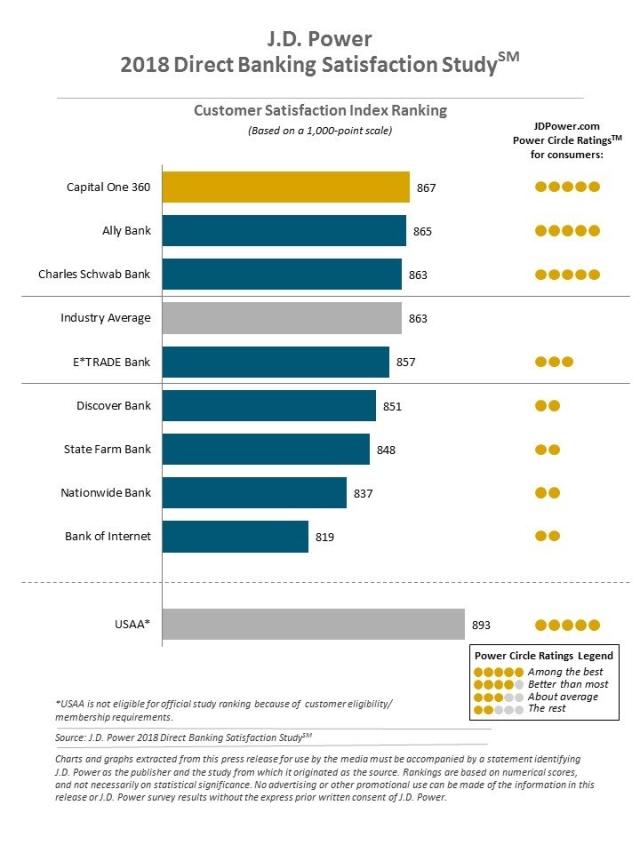

- Direct banks outperform traditional retail banks: The overall satisfaction score for direct banks is 863 (on a 1,000-point scale), which is 57 points higher than the overall satisfaction score for traditional branch-based retail banks as found in the JD Power 2018 U.S. Retail Banking Satisfaction Study.SM

- Mobile poses a challenge: More than three-fourths (77%) of direct bank customers indicate using the mobile channel (an increase of 5 percentage points from last year), and customer satisfaction with the mobile channel has declined 8 points from last year, making it the channel with the narrowest performance lead compared to retail banks. The performance gap in mobile customer satisfaction between direct banks and traditional retail banks is just 14 points.

- Majority still treat direct banks as secondary banking provider: Just 43% of direct bank customers consider their direct bank to be their primary bank. Overall satisfaction among that 43% is 873, which is 18 points higher than among customers who consider their direct bank to be a secondary banking relationship. Primary banking customers are more engaged, making an average of 41 contacts with their bank vs. 21 contacts for secondary customers.

- Social media is key marketing channel for direct banks: Among direct bank customers who opened a new product in the past 12 months, 38% say they were influenced by social media to open the new product. Approximately 50% of Gen Y,[1] Gen Z and mass affluent[2] customers cite social media as being influential.

Study Rankings

Capital One 360 ranks highest in overall satisfaction with a score of 867. Ally Bank (865) ranks second and Charles Schwab Bank (863) ranks third.

The U.S. Direct Banking Satisfaction Study, now in its second year, measures overall satisfaction with direct banks based on five factors (in order of importance): channel activities; products and fees; communication; new account opening; and problem resolution. The channel activities factor includes five subfactors: online banking website; mobile banking; assisted online; live phone; and automated phone. The study is based on responses from 2,709 direct bank customers nationwide and was fielded in April 2018.

To learn more about the U.S. Direct Banking Satisfaction Study, visit http://www.jdpower.com/business/resource/us-direct-banking-satisfaction-study.

JD Power is a global leader in consumer insights, advisory services and data and analytics. These capabilities enable JD Power to help its clients drive customer satisfaction, growth and profitability. Established in 1968, JD Power is headquartered in Costa Mesa, Calif., and has offices serving North/South America, Asia Pacific and Europe. JD Power is a portfolio company of XIO Group, a global alternative investments and private equity firm headquartered in London, and is led by its four founders: Athene Li, Joseph Pacini, Murphy Qiao and Carsten Geyer.

Media Relations Contacts

Geno Effler; Costa Mesa, Calif.; 714-621-6224; [email protected]

John Roderick; St. James, N.Y.; 631-584-2200; [email protected]

About JD Power and Advertising/Promotional Rules www.jdpower.com/business/about-us/press-release-info

[1] JD Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2004). Xennials (1978-1981) and Millennials (1982-1994) are subsets of Gen Y.

[2] JD Power defines a mass affluent customer as one with a household annual income of $150,000 or more and investable assets less than $250,000, or household annual income less than $150,000 and investable assets of $100,000 or more.