COSTA MESA, Calif.: 27 Oct. 2016 — Fast-growing small businesses create both an opportunity and a threat for their banks, according to the JD Power 2016 U.S. Small Business Banking Satisfaction Study,SM released today.

Small businesses that are growing sales 20% or more annually are considerably more satisfied overall with their banking experience than their counterparts at small businesses with lower or no annual growth (844 vs. 781, respectively, on a 1,000-point scale).

Yet the study finds that 22% of the fast-growing small businesses have switched banks in the past 12 months, compared with only 5% of the other small businesses. Perhaps even more concerning to banks is that 25% of owners of fast-growing small businesses indicate they intend to switch within the next year, while only 7% of other small businesses indicate the same.

“If the business is growing, the owner is more likely to need new loans and banking products, and that makes them look around at other options,” said Jim Miller, senior director of banking at JD Power. “Once they start exploring, it often doesn’t take long to move from considering switching banks to actually switching. For the banks, that means the risk of potentially losing customers, but it also creates the opportunity to acquire new customers from competitors. It’s critical that the banks consistently communicate the other products and services they have to help businesses continue to grow.”

Fast-growing small businesses are very sensitive to problems: when they experience one or more problems, their likelihood to switch more than doubles, to 57% from 24%. Applying for a loan is also a critical “moment of truth” for these customers, with 61% of fast-growing businesses that applied for a loan in the past year considering switching, compared with 19% of those that have not applied for a loan considering the same. The need for loans opens the door to competition, with 73% of fast-growing businesses considering a non-bank alternative. To compete, banks need to offer an easy loan application process, which is an area of opportunity, as only 49% of loan applicants say that applying for a new loan was “very easy.”

“Banks need to be proactive in order to retain fast-growing small businesses,” said Miller. “To retain their business, it is critical to develop a strong relationship before they need a loan or experience a problem. Banks can do this through proactive outreach, understanding their business and providing advice.”

Other key findings of the study include:

- First Impression Is Critical: Account initiation is the bank’s first interaction with a new customer. Among small business owners who recently opened a new account, 74% say the bank representative “completely” identified their needs before recommending a product; 62% say the representative explained fees and pricing; and 44% say the representative provided information on other products.

- The Digital Edge: Big banks1 lead the way in providing digital channel solutions for their small business customers. Big banks outpace regional and midsize banks in terms of having the highest percentages of small business banking customers using mobile banking, online expense tracking and online financial management tools. Additionally, big banks have higher customer satisfaction with both their online and mobile banking experiences, compared with regional and midsize banks.

- Small Business Owner Diversity: Among the diverse groups of small business owners, Millennial2 owners have the highest overall satisfaction (863), followed by minority owners (843) and female owners (803). Conversely, Millennial owners are the most likely to say they “definitely will” switch banks (26%), followed by minority owners (21%) and female owners (10%).

The study, now in its 11th year, measures small business customer satisfaction with the overall banking experience by examining eight factors: product offerings; account manager; facility; account information; problem resolution; credit services; fees; and channel activities. Satisfaction is calculated on a 1,000-point scale.

Small Business Banking Satisfaction Rankings

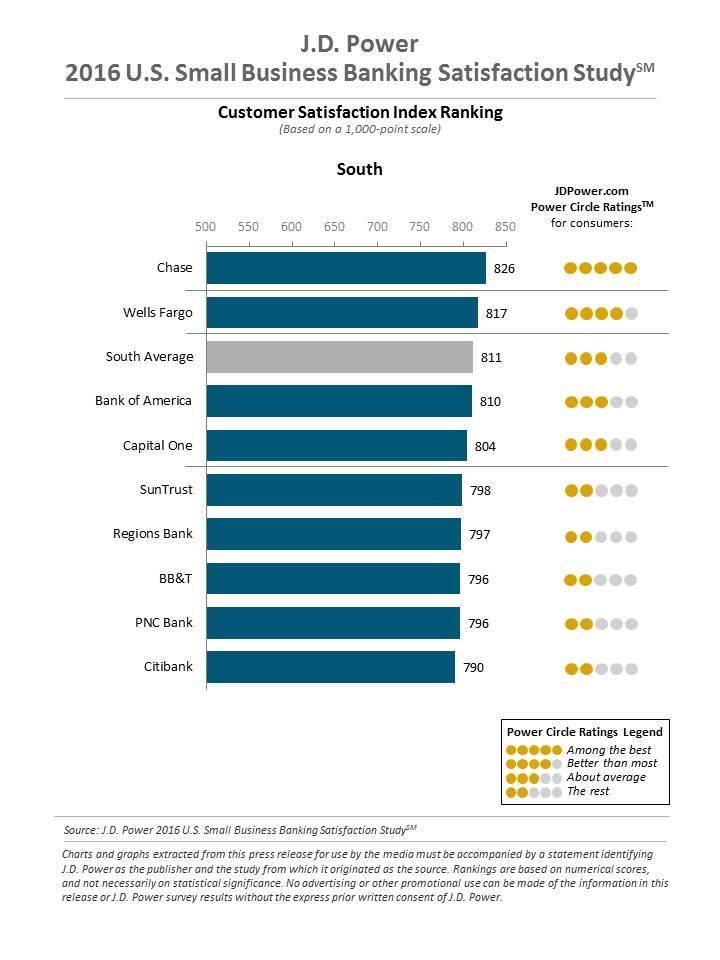

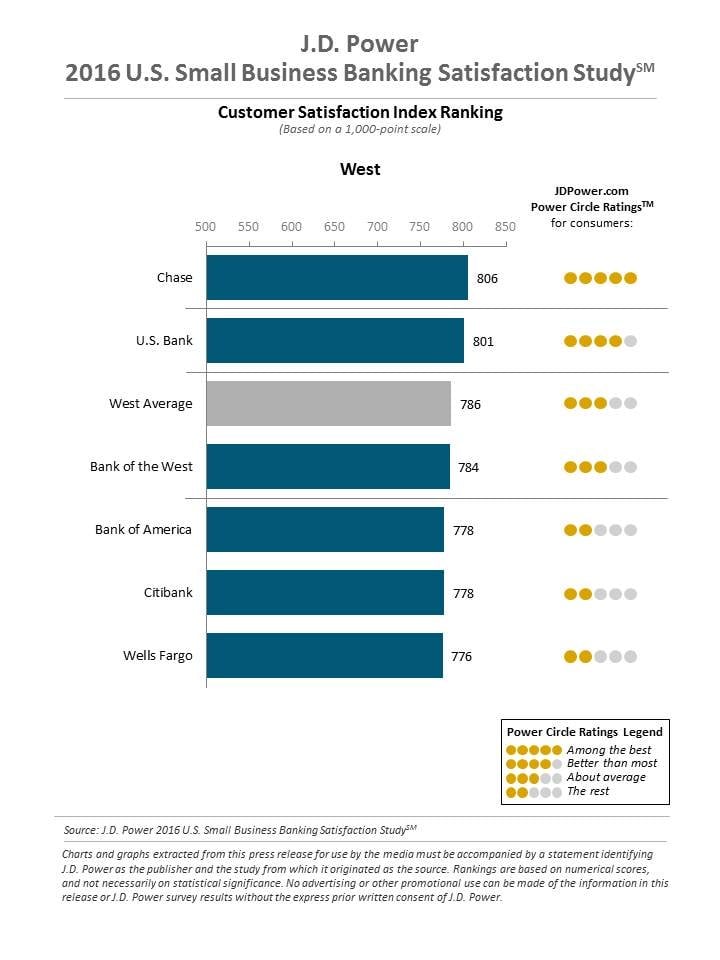

Chase ranks highest in small business banking satisfaction in the West region for a fourth consecutive year, with a score of 806, and in the South region with a score of 826. Chase is followed in the West region by U.S. Bank (801), and is followed in the South region by Wells Fargo (817).

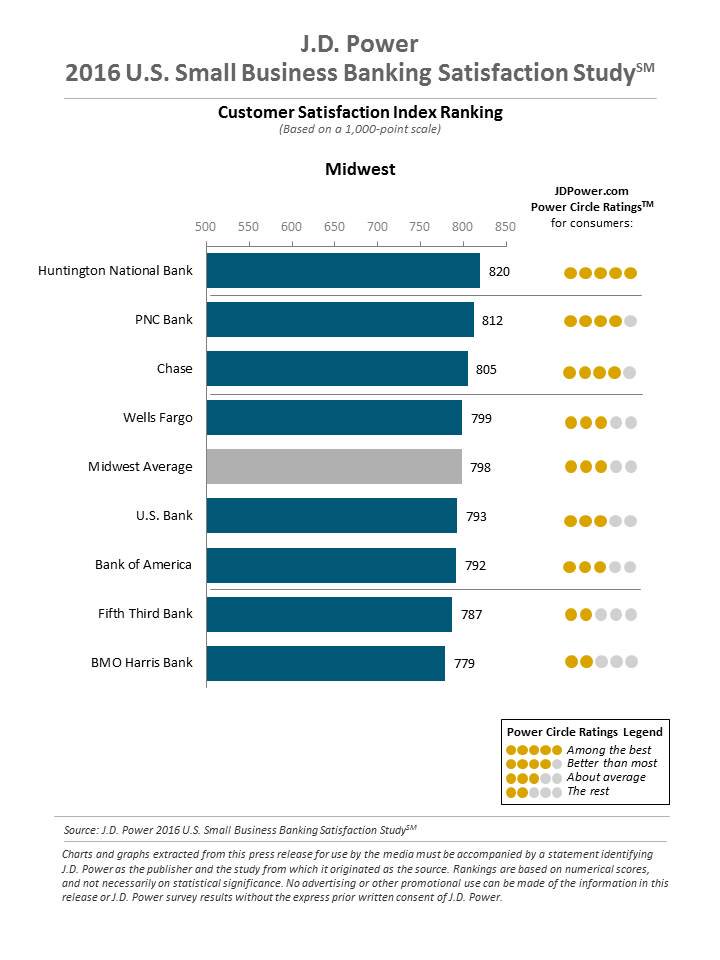

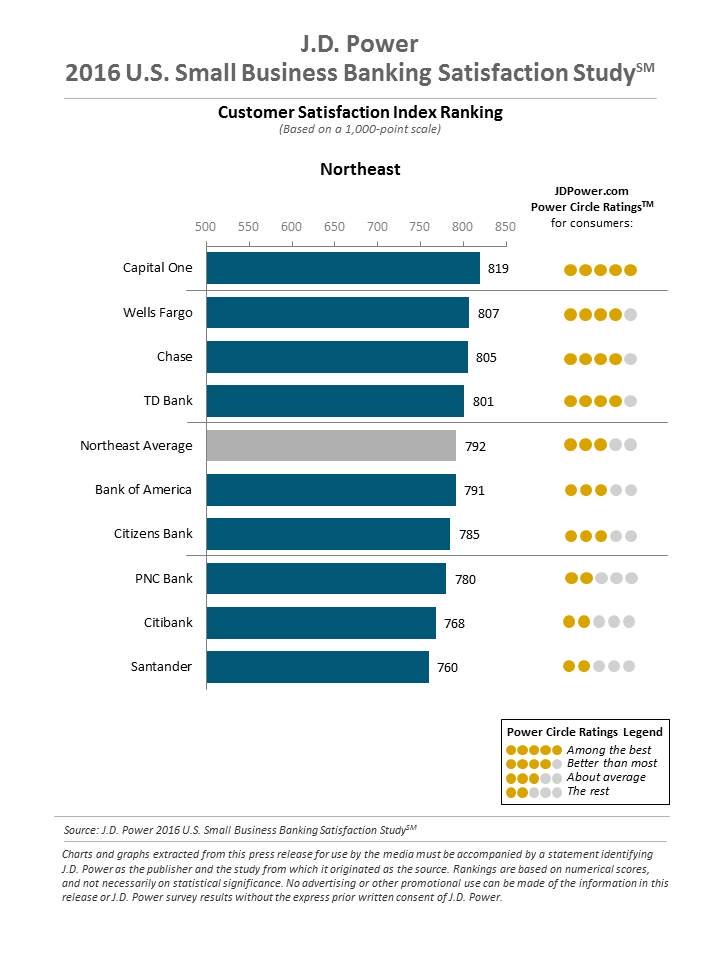

Capital One ranks highest in small business banking satisfaction in the Northeast region with a score of 819. Wells Fargo ranks second (807) and Chase third (805). Huntington ranks highest in the Midwest region with a score of 820, followed by PNC Bank with 812 and Chase with 805.

The 2016 U.S. Small Business Banking Satisfaction Study includes responses from 8,159 small business owners or financial decision-makers who use business banking services. The study was fielded from June 2016 through mid-August 2016.

For more information about the 2016 U.S. Small Business Banking Satisfaction Study, visit http://www.jdpower.com/resource/us-small-business-banking-satisfaction-study.

See the online press release at http://www.jdpower.com/pr-id/2016212.

Media Relations Contacts

John Tews; Troy, Mich.; 248-680-6218; [email protected]

Geno Effler; Costa Mesa, Calif.; 714-621-6224; [email protected]

About JD Power and Advertising/Promotional Rules www.jdpower.com/about-us/press-release-info

1. Big banks are defined as the six largest financial institutions based on total deposits as reported by the FDIC, averaging $180 billion and above. Regional banks are defined as those with between $180 billion and $33 billion in deposits. Midsize banks are defined as those with between $33 billion and $2 billion in deposits.

2. JD Power defines Millennials as born in 1982 through 1994.