Banking and Payments Intelligence Report

Novelist Patrick Rothfuss once wrote, “Time and tide make us mercenaries all,” words that accurately describe the relationship between banks and their customers in the time of a 40-year-high inflation rate.

As Americans find that their paychecks don’t quite put as large of a dent in their bills and their retirement accounts are struggling to keep pace, they are actively starting to look for ways to make their money stretch further, casting aside their long-standing loyalties along the way.

When it comes to retail banking customers, that trend is manifesting itself in a hunt for bigger incentives at new institutions, a development that—even in a time of waning brand loyalty—has gathered momentum quickly during the past several months.

Money on the Move

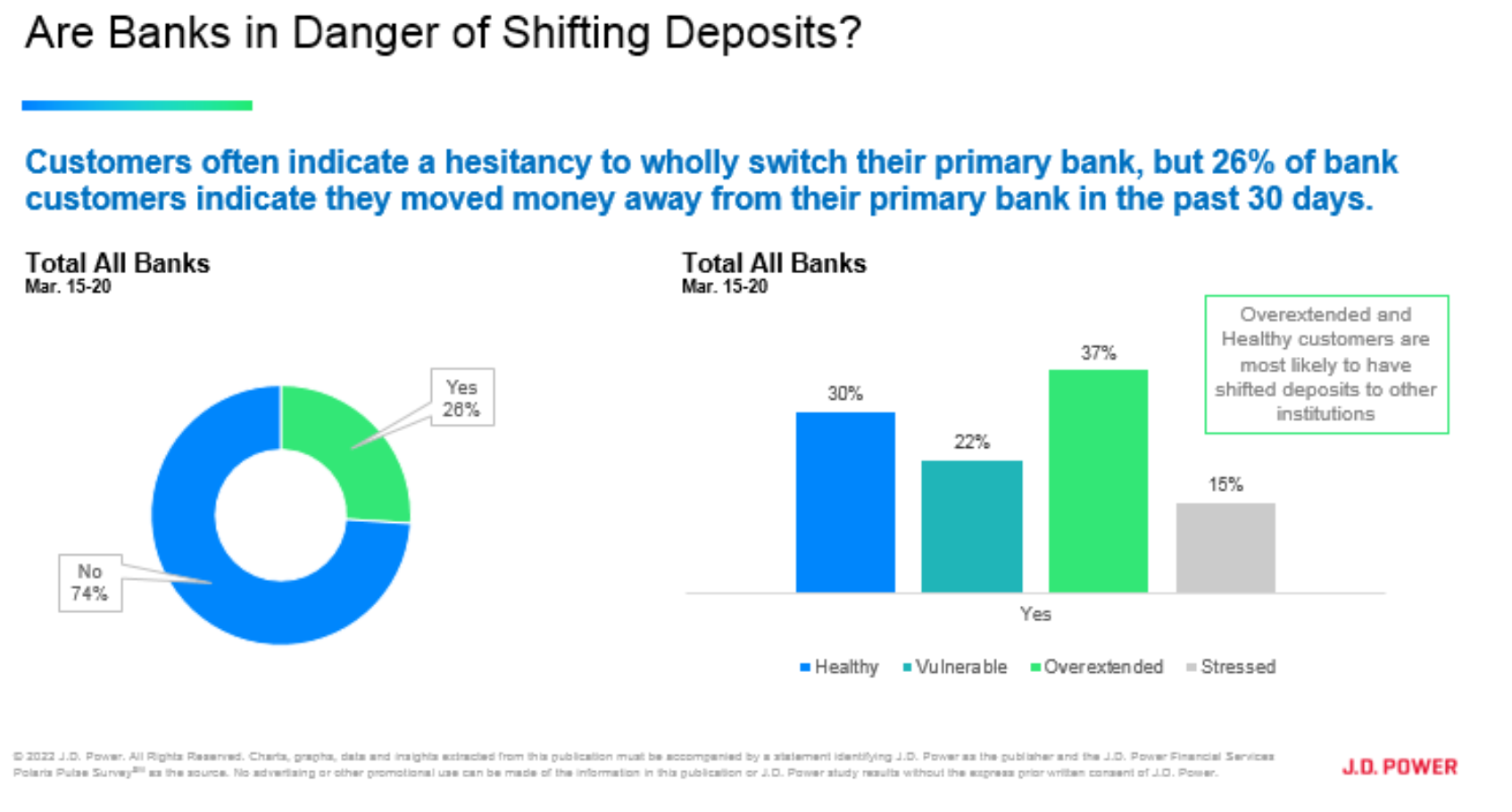

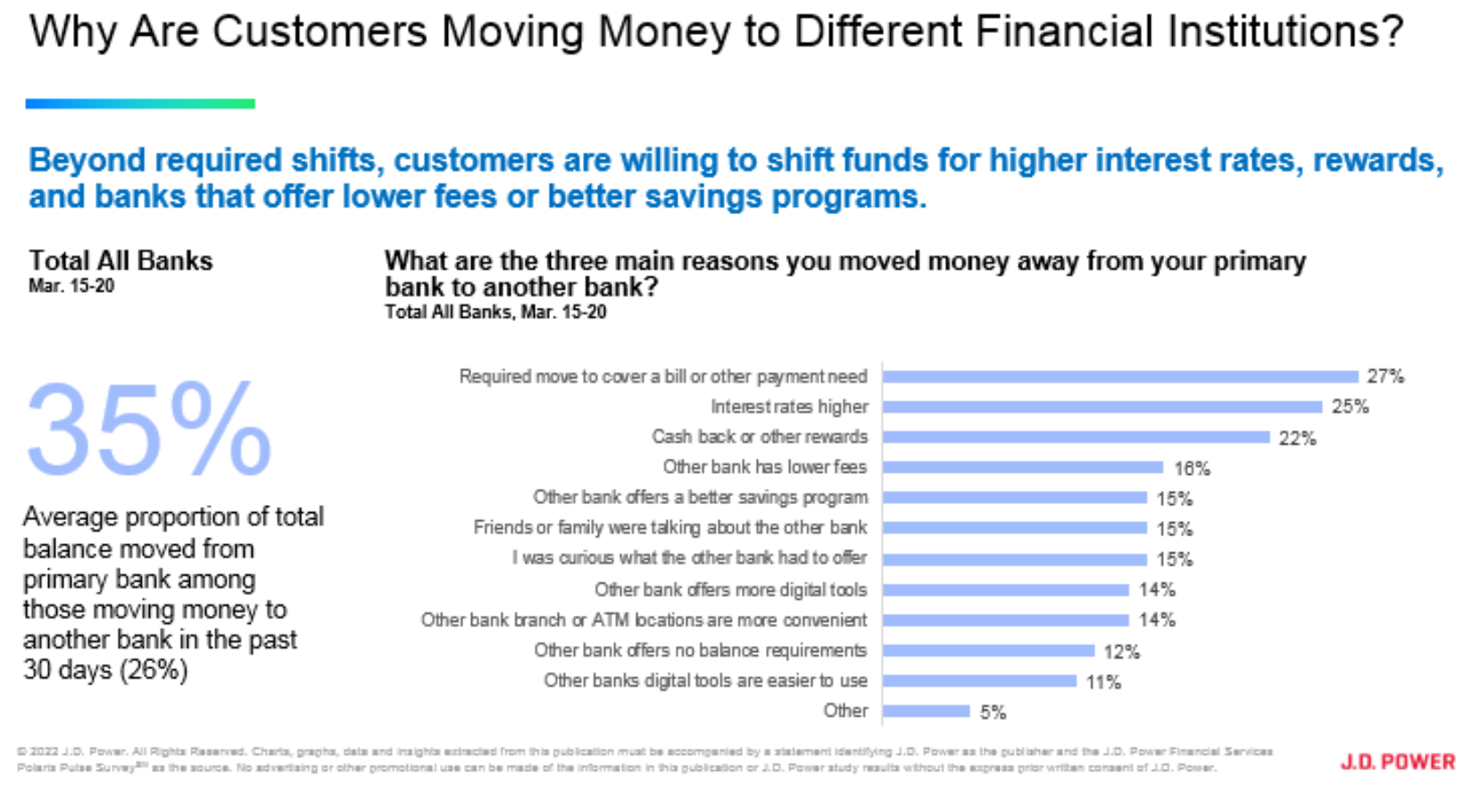

The trend is clear: Americans are tightening their belts, and they’re willing to reset that “Customer Since” line on their monthly statements to do it. In fact, we’ve found that 26% of customers moved money to another institution in the past 30 days and, on average, they moved about one-third of their deposits.

Banking customers under age 40 are more likely to have shifted money in the past 30 days, as well as customers who are in more vulnerable states of financial health—but the trend is not exclusive to these segments. Customers in healthy financial situations are on the move as well, which creates a huge opportunity for banks to get aggressive about customer acquisition.

The Rain-Making Factors

As banks begin to sit up and take notice of this trend, they must be mindful of the specific incentives that are making Americans take this unfamiliar leap.

While it’s true that some movement is being driven by specific bill-paying requirements (e.g.,, a customer moving a money from a bank to a credit union that holds the note on his or mortgage), just as many customers are using this time of financial flux to get savvy about hunting for higher interest rates on their savings, lower fees and cash back offers.

While these products are driving factors, customers are also swayed by friends and family recommendations and a general curiosity about other offerings.

The Spending Shift

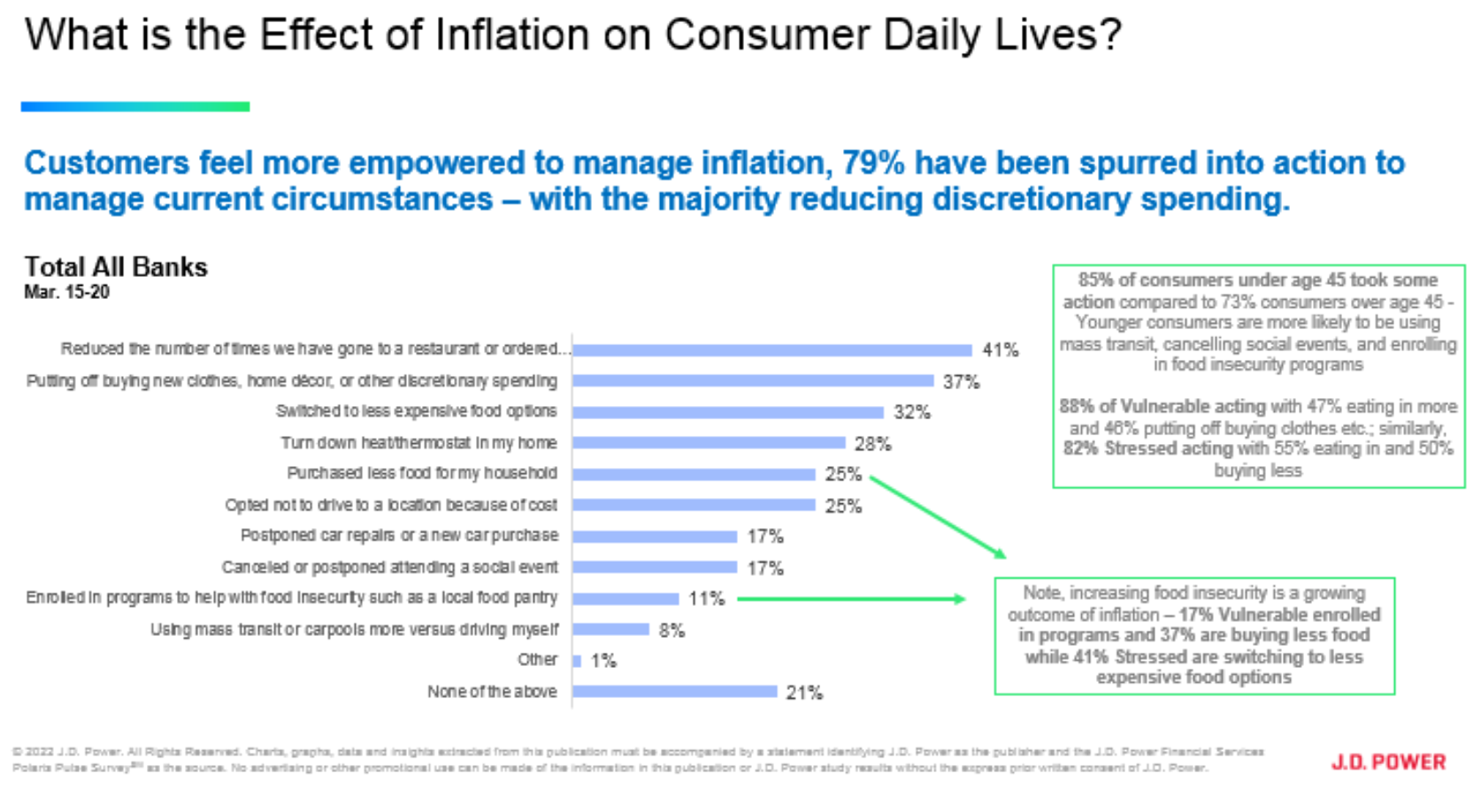

Americans aren’t just making changes to their banking. Customers surveyed also say they are revamping their discretionary spending.

Overall, 85% of customers under the age of 45 say they have made a change in their spending habits to combat inflation, compared with 73% of customers over age 45. Among those who have changed their spending habits, 41% say they have reduced the number of times they have gone to a restaurant or ordered takeout, 37% have put off buying new clothes or home décor, and 28% say they have fiddled with their thermostat settings to offset energy costs.

Building Meaningful Digital Customer Experiences

All of this, of course is set against a backdrop of massive digital transformation in America’s retail banks, wherein most consumer transactions with retail banks are occurring online or on mobile apps. As we reported in the JD Power 2022 U.S. Retail Banking Satisfaction Study,SM many banks have struggled to differentiate and deliver meaningful customer experiences via digital channels.

In fact, we found that traditional success metrics like speed, efficiency and convenience were no longer top priorities for banking customers. The one factor that does heavily influence customer experience in this environment is the bank’s ability to “support the customer during challenging times.” We found that customer satisfaction with retail banks rises 155 points (on a 1,000-point scale) when customers indicate that their bank supports them during challenging economic times. Similarly, 63% of customers say they “definitely will not” switch banks and 78% say they “definitely will” reuse their bank when it delivers this support. However, despite its huge effect on customer satisfaction, only 44% of banks are delivering on this metric.

We are living in one of those challenging times right now. For banks that want to seize this moment to win new customers and build loyalty among existing ones, the status quo will not due. They will need to connect with customers, delivering the right combination of financial incentives, personalized financial advice, hands-on help with problem resolution and guidance on how to grow their money.

Find Out More

To learn more about the underlying research behind this industry briefing or schedule an interview with Jennifer White, please contact the numbers below.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]