Remember Blockbuster? The ubiquitous video rental stores have now become a universal symbol of disruption. But it wasn’t just the advent of streaming that broke the video rental giant. Years before anyone had figured out how to host a massive movie catalog in the cloud and stream it to smart TVs, Netflix’s big innovation was sending DVDs through the mail and letting customers keep them as long as they wanted. That simple twist on the old model—direct delivery with no late fees—was the real breakthrough that delighted customers and made Blockbuster’s brick-and-mortar model, which generated roughly 16% of annual revenue in late fees, seem antiquated overnight.

A very similar pattern has been playing out in the retail banking industry for the past few years. A combination of historically low interest rates, reduced use of brick-and-mortar branches and the introduction of countless digital payment services like Venmo, Apple Pay and Zelle have given retail bank customers reason to question the value of their traditional banking relationships. On top of that, increased regulatory pressures have challenged banks to rethink many of their tried-and-true business practices.

Unlike Blockbuster, however, retail banks have not ignored the trend. Recent moves by Ally, Capital One and Bank of America to abandon or dramatically lower overdraft and other fees are the latest in a series of significant moves retail banks have made to adjust their strategies in line with the evolution of the marketplace. The decision to move from a punitive, carrot-and-stick approach suggests that retail banks are recognizing that the role they play in their customers’ lives needs to evolve beyond service provider and into more of a hub of financial advice and guidance. And that may just be the key to staying relevant amid growing threats from FinTechs.

The Rise of the Benevolent Banker

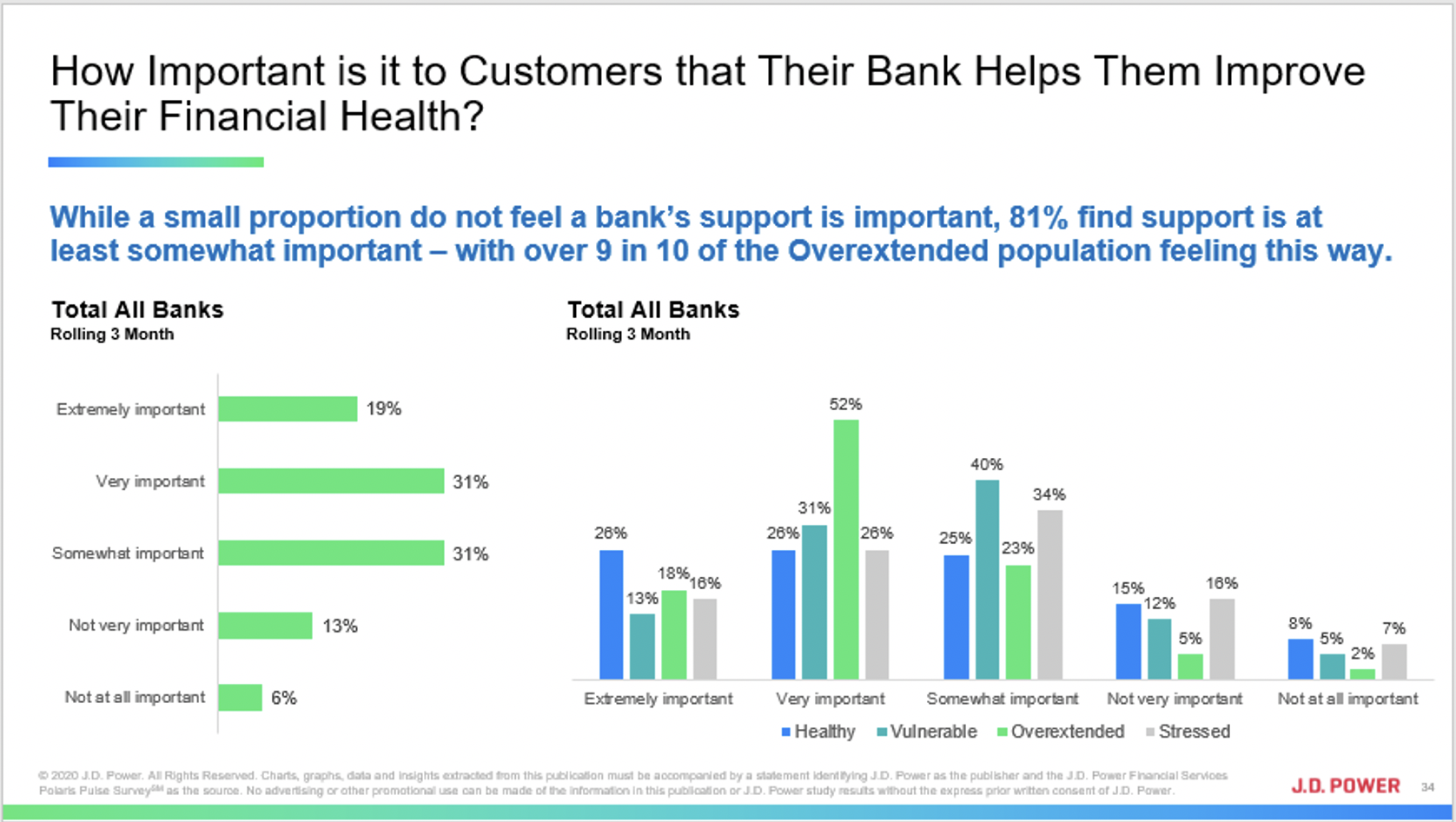

In fact, according to new data surfaced in the JD Power Financial Health and Advice Program, 81% of retail bank customers say they feel strongly that banks are in a position to help them improve their overall financial health. Moreover, our 2021 U.S. Retail Banking Advice Satisfaction Study found that overall customer satisfaction increases 229 points (on a 1,000-point scale) when customers are offered advice/guidance that completely meets their needs.

On the flip side of that phenomenon, our data shows that retail bank customers are more than twice as likely to switch banks if they’ve been charged a fee of any kind at any point over the last three months versus customers who have not been charged any fees. Across every metric—customer satisfaction, Net Promoter Score (NPS)1, customer engagement—punitive bank fees have a significant negative influence on customers’ relationships with their banks.

Banks have begun to recognize this and many of the largest national retail banks have launched initiatives focused on delivering personalized advice to customers. These efforts are paying off, too. The top four performing banks in our U.S. Retail Banking Advice Satisfaction Study last year were all national banks.

Uneven Recovery Puts Spotlight on Fees and Advice

The U.S. economy may be in a recovery, but the K-shaped nature of that recovery means that it is playing out unequally for different economic groups. In fact, while banking customers may no longer find themselves on the brink of ruin the way they were in early 2020, many of the existing financial problems that existed prior to the pandemic are still prevalent.

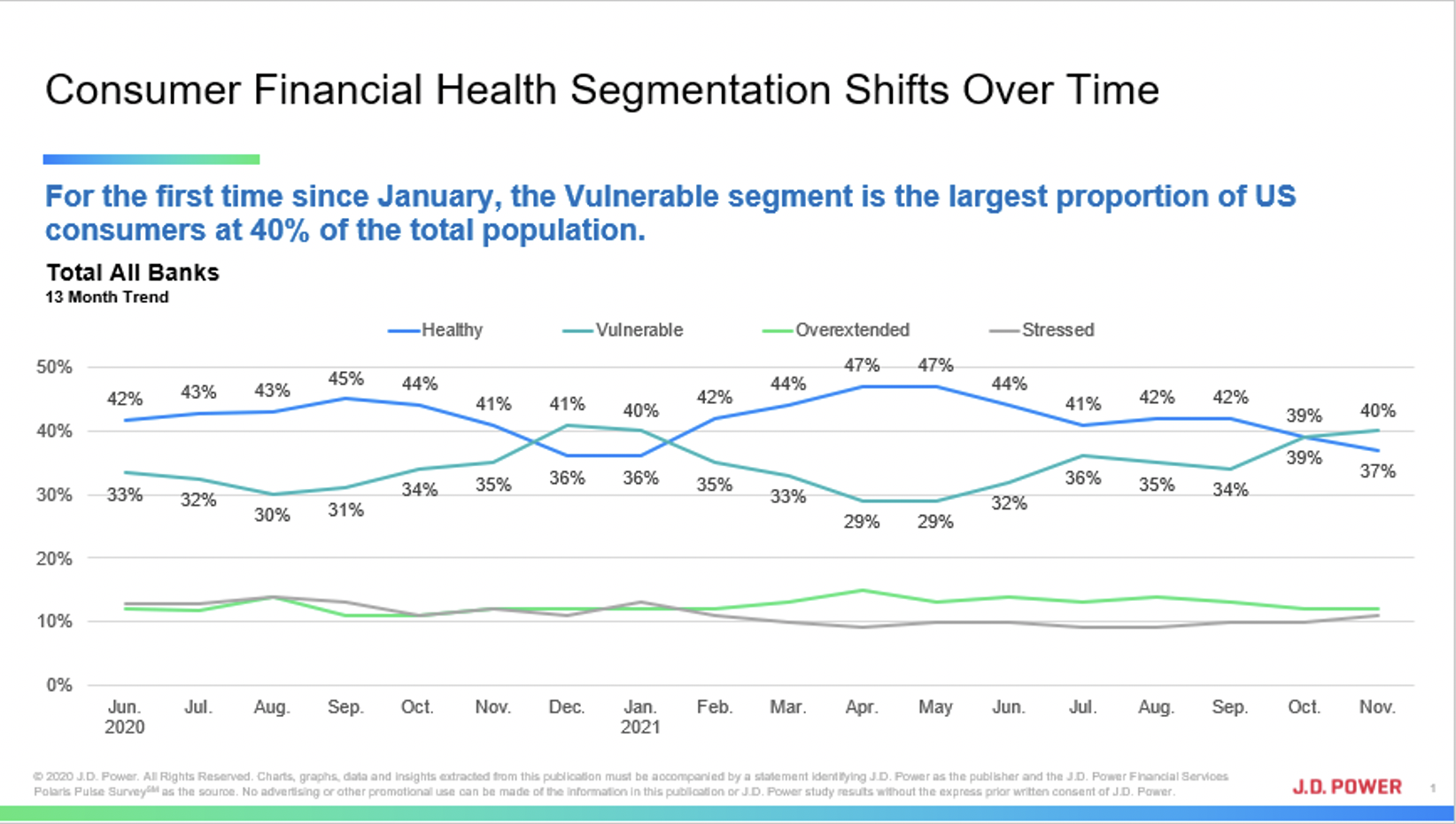

As of November 2021, just more than one-third (37%) of retail bank customers are classified as financially healthy, according to JD Power data. The largest segment of retail bank customers (40%) is classified as vulnerable, while 12% fall into the overextended category and 11% are stressed.

This economic backdrop is critical context for the recent announcements by major banks to remove or dramatically lower overdraft fees. Our Retail Banking Study data indicates that, during the last three months, 4% of healthy customers paid overdraft fees while 18% of the vulnerable segment owed the bank money due to overdrafts. There is limited variation between the overextended (7%) and stressed (8%) populations, but they are still paying overdraft fees at twice the rate of the healthiest banking customers. By eliminating these fees, Ally, Capital One and Bank of America are not only ensuring that all consumers are treated equally, but they are addressing the difficult circumstances through which many customers are currently living.

Seizing the Moment

The nation’s retail banks have been remarkably nimble and sensitive to customer sentiment during the pandemic. By the end of 2021, a record 41% of retail customers were digital-only and, although 24% of customers said they are worse off financially, overall satisfaction with retail banks increased. That’s because 63% of retail bank customers said their banks completely supported them during the pandemic, which drove an 86% increase in likelihood of reusing that bank; a 60-point increase in NPS®; and a 48% decrease in problems or complaints. Specific bank actions that customers associate with support during the pandemic are waiving charges/fees; supporting the community; offering additional advice/guidance; and providing late payment forgiveness.

The current trend toward fee reduction or removal is an important part of that evolution and may just go down in history as the tipping point when retail banks successfully averted the threat of disruption by putting their customers’ needs ahead of short-term revenue.

Methodology

This JD Power Retail Banking Insight is based on data collected as part of the JD Power Financial Health and Advice Program, the JD Power U.S. Retail Banking Satisfaction Study and the JD Power U.S. Retail Banking Advice Satisfaction Study.

Find out More

This JD Power Retail Banking Insight was authored by Jennifer White, senior consultant, financial services intelligence, at JD Power. Please contact us at the numbers below to learn more about the underlying research.

Media Contacts:

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

1 Net Promoter,® Net Promoter System,® Net Promoter Score,® NPS,® and the NPS-related emoticons are registered trademarks of Bain & Company, Inc., Fred Reichheld and Satmetrix Systems, Inc.