Banking and Payments Intelligence Report

May 2024

Leveling Out

While customers’ financial health has seen gradual improvement over the last six months, the changes are modest. Nearly one-third (32%) of respondents are financially healthy, while 43% fall into the vulnerable category. This stabilization reflects a certain acceptance of the current economic landscape.

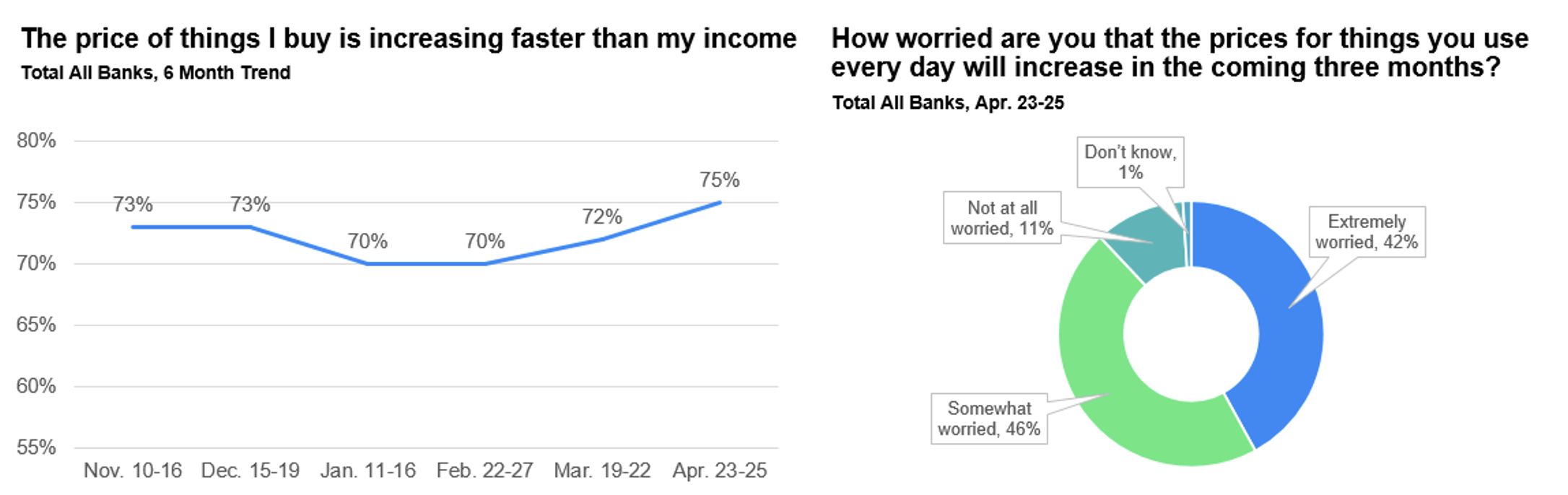

While there may be acceptance, there is palpable uneasiness about managing inflation. Three-fourths (75%) of bank customers say that the cost of goods is increasing faster than their income and 42% are extremely worried prices for goods they use every day will increase in the next three months. Those figures both reflect the highest level observed in the past six months.

All Dried Out

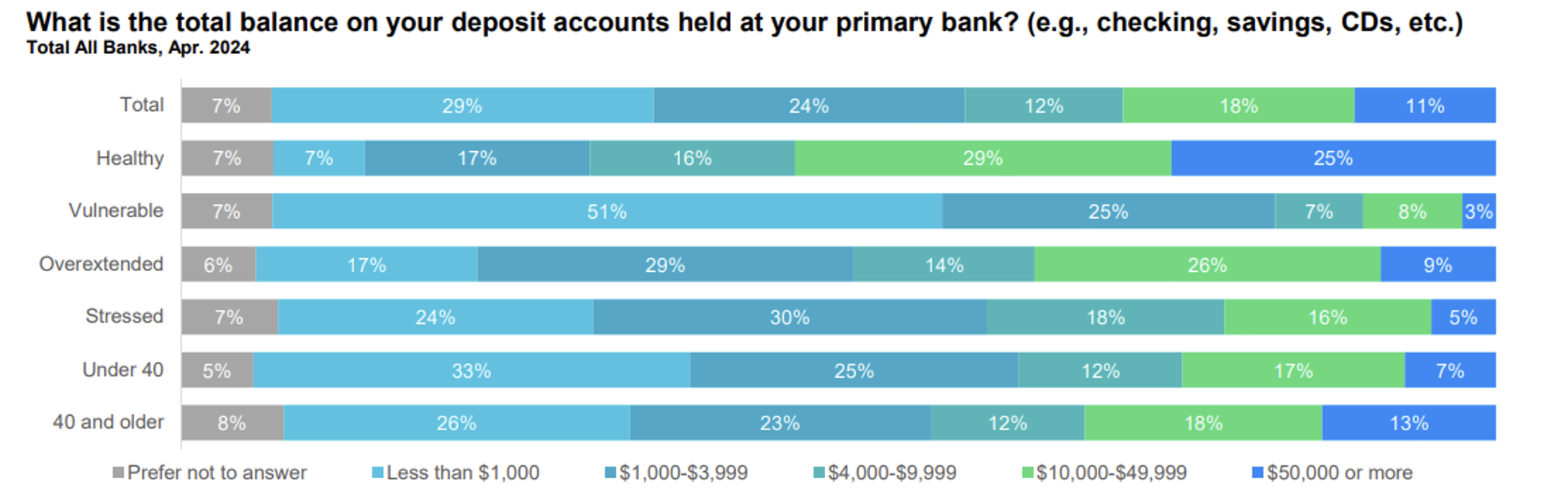

That worry is likely a reflection of how much—or how little—liquidity bank customers currently have on hand. More than half (53%) of customers have less than $4,000 in their primary deposit accounts.

Interestingly, having a higher deposit level does not guarantee financial health. When asked about their deposits at their primary bank, 29% of healthy customers said they had between $10,000 and $49,999 on deposit compared with 26% of customers in the overextended category and 16% in the stressed category.

The Search for Higher Yields

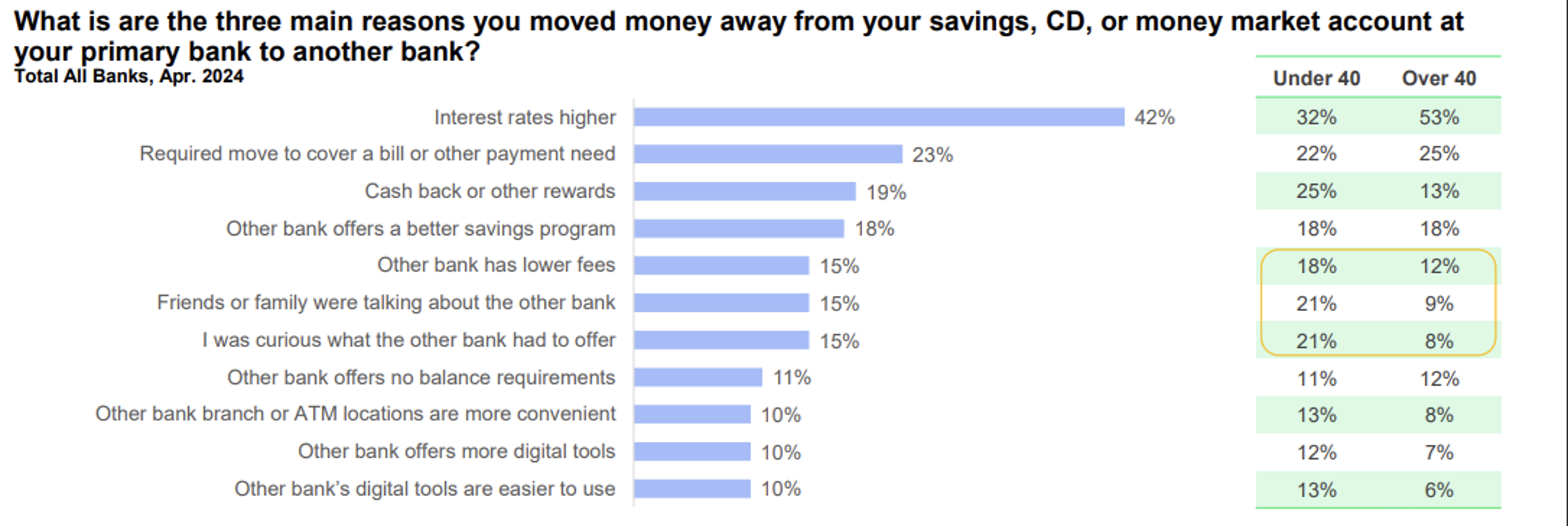

To combat these concerns about funds, some bank customers have begun to shift their money from their primary bank to another institution often seeking to earn as much as possible. Overall, 22% said they have moved money from their primary bank shifting one-third of their deposits. This rate is highest among customers in the overextended category.

When asked why they moved their funds, some were required to make moves but among those choosing to shift deposits 42% said higher interest rates and cash back or other rewards (19%). Overall, 40% of primary savings customers earn less than 1% APY on their money, while 23% do not know what their savings interest rate is. This means there are some savvy customers taking advantage of current high interest rates to help grow their money, but a large portion are not making these money moves.

Chartering New Territory

While customers try to navigate the next phase of a very uncertain economic landscape, they are going to be on the hunt for any way they can gain an edge. Whether that’s a loan product, budgeting tools, or higher interest rate accounts, more customers than ever before are willing to test waters with banks both new and familiar.

That means that there is not only a need for more proactive customer engagement, but also an opportunity to help customers through a time of great stress. For banks willing to offer higher yield accounts, they have the potential to coax a lot of new business through the doors and, if done properly, convert that new business into long-lasting relationships.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in April 2024. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]