Banking and Payments Intelligence Report

April 2023

Recent Bank Failures Strain Consumer Faith in U.S. Banking System

As if inflation and fear of a recession weren’t enough to stoke the fears of banking customers in the United States, a new concern has emerged: The overall stability of the U.S. banking system.

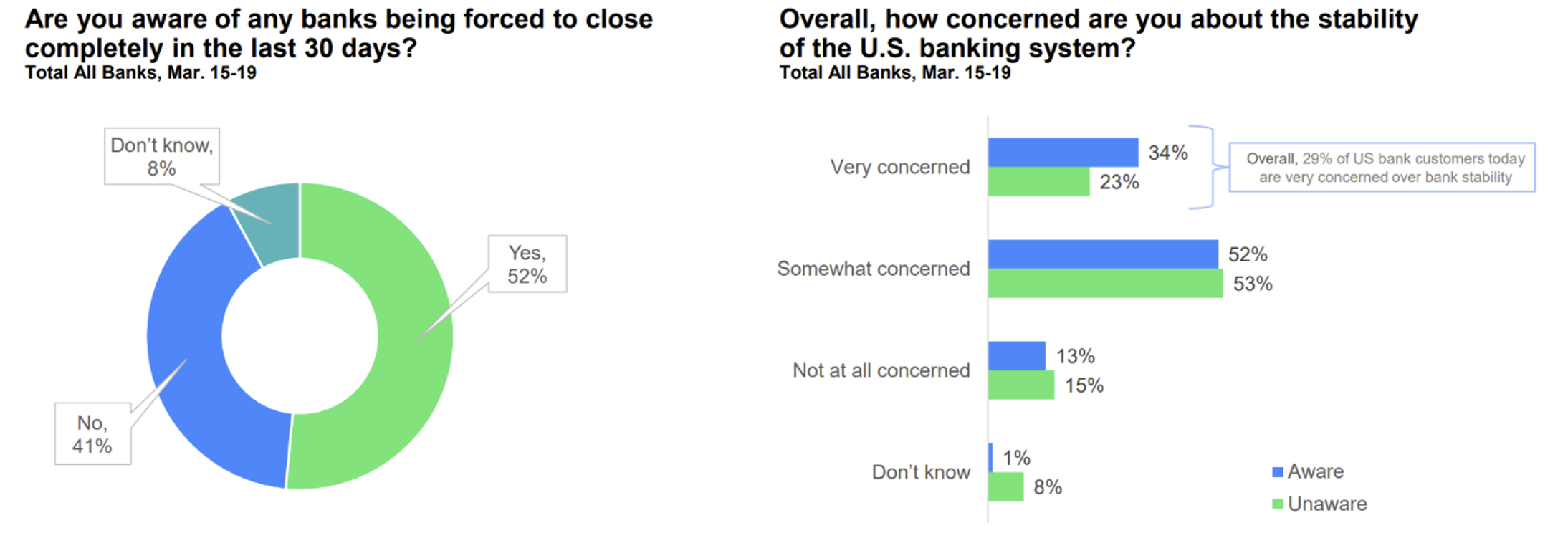

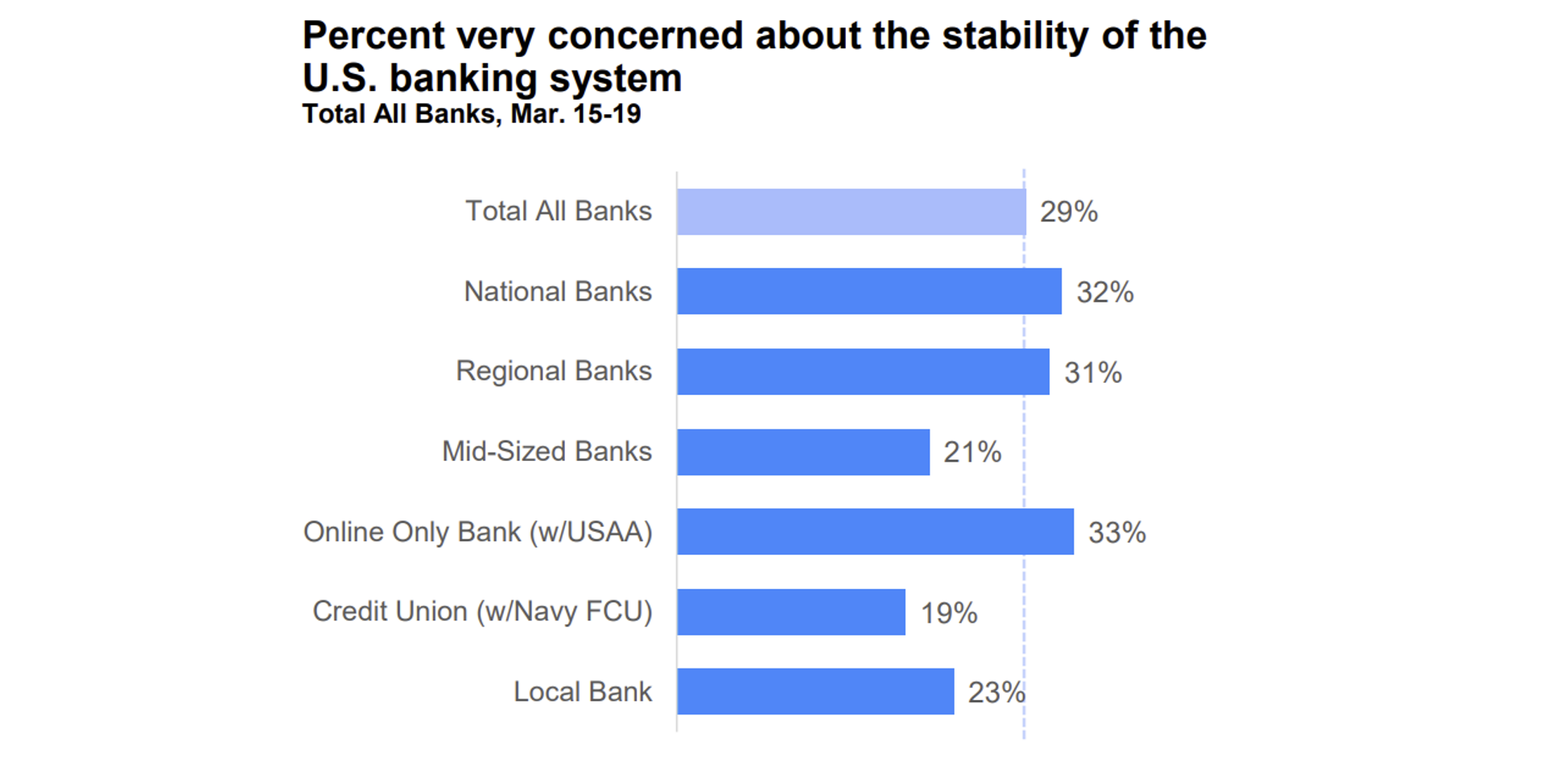

According to the latest JD Power data, nearly one-third (29%) of banking customers say they are “very concerned” with the stability of the banking system. Among those who are aware of the recent Silicon Valley Bank and Signature Bank failures, that number rises to 34%. Overall, customers with higher total deposits and higher financial health scores[1] show more concern about the stability of their banks and the safety of their deposits.

The high-profile bank failures have also stoked misconceptions among retail bank customers about bank failure risk and deposit protection. Notably, consumers banking with smaller, regional and mid-sized banks show consistently lower levels of concern about bank stability than those banking with larger, national institutions.

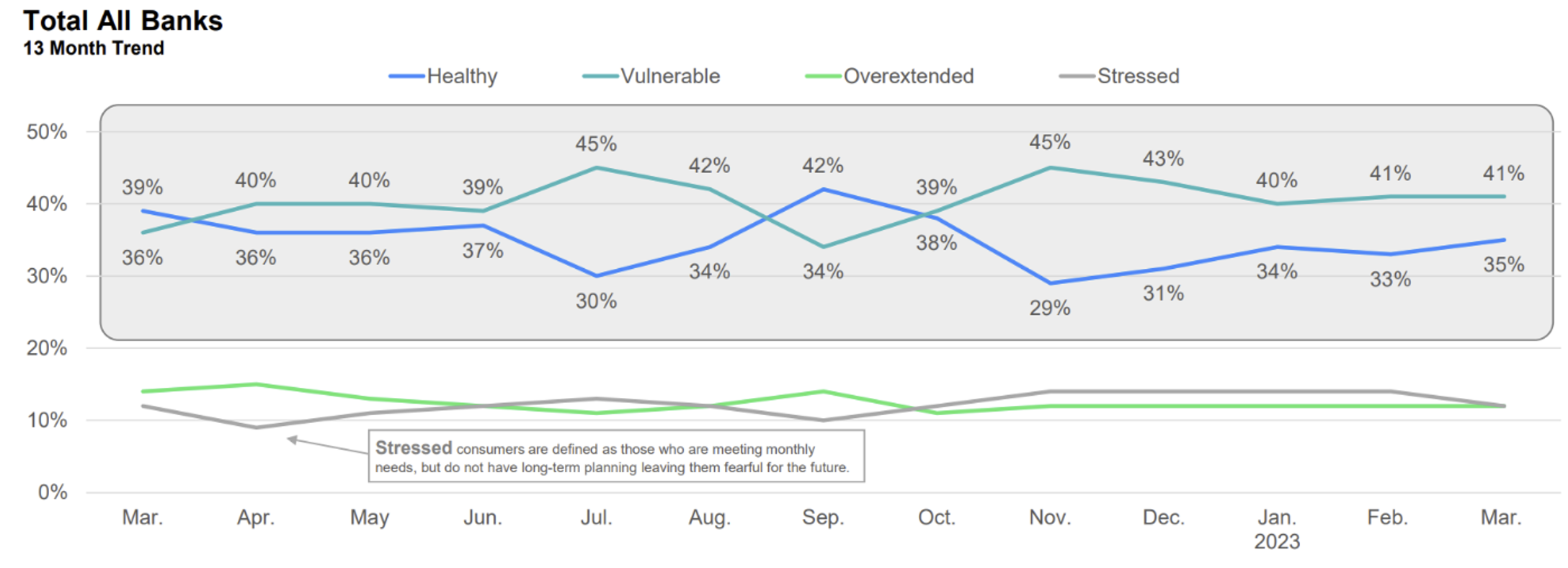

Overall Financial Health Holds Steady

For the third straight month, there has been no noteworthy change in overall financial health. More than one-third (35%) of respondents are financially healthy, while 41% are vulnerable.

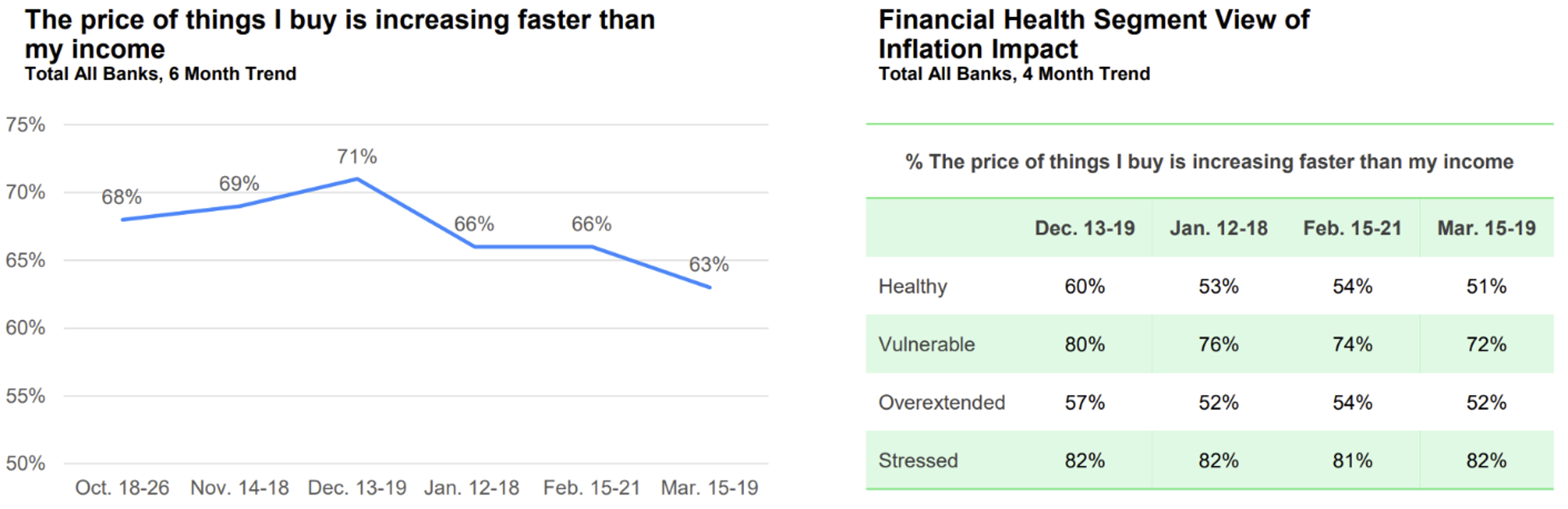

The overall level of inflation recognition fell slightly to 63%. The percentage of customers that said the price of goods is increasing faster than their income also fell slightly for most customer segment groups but was largely in line with the previous months as well.

Unpacking Bank Customer Fears

The failures of Silicon Valley Bank and Signature Bank have given some banking customers a case of 2008 déjà vu.

Overall, 29% of banking customers say they are “very concerned” about the stability of the U.S. banking system. That number increases to 34% among customers who are aware of the Silicon Valley Bank and Signature Bank failures. Just over half (52%) of banking customers are aware of any bank being forced to close.

Banking customers who are more likely to be aware of the collapse are financially healthy, more than 40 years old, and have more than $10,000 in deposits.

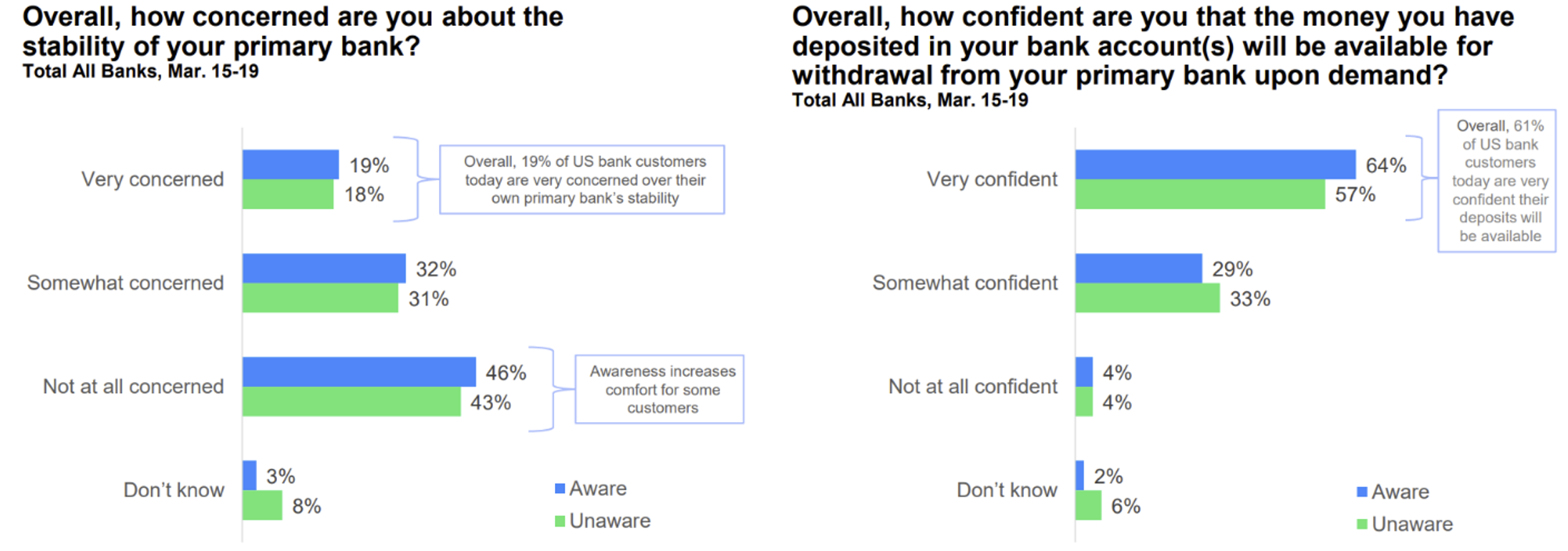

Interestingly, when asked about their specific bank, the level of customer concern falls from 29% to 19%, indicating that most customers view bank stability as someone else’s problem.

The survey also uncovered some widespread misconceptions among customers about which banks have the largest risk exposures. Customers of large, national banks express the second-highest level of concern (32%), even though those banks that are actually more protected. Conversely, local bank customers (23%), mid-sized bank customers (21%) and credit union members (19%) had the three lowest levels of concern, while those institutions have the bigger risk exposure.

Cash Under the Mattress?

As customers contend with this new anxiety, will it lead to a mass exodus of deposits? Not necessarily. Overall, 17% of bank customers say they are very likely to switch banks in light of the recent bank failures. When asked about deposits, that number increases slightly to 23%, suggesting that customers are more likely to explore relationships with secondary banks than to completely exit their primary institutions.

A Call for Customer Education

Bank customers are looking for guidance and now is a vital time to educate them about the ins and outs of FDIC insurance, restore confidence by outlining safeguards currently in place and deliver personalized messages that speak to their individual financial situations. By being transparent about risk and how best to protect a customer’s financial interest, banks will not only build a base that is more informed, but also one that is more confident and loyal.

It is also noteworthy that the customers who are most concerned are those with the highest deposits and strongest levels of overall financial health—in other words, the banks’ best customers. If banks want to retain these customers, they’ll need to help them understand the challenge at hand, and the steps they are taking to navigate through it.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in March 2023. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.