Inflation is the bugaboo that just won’t go away. As the U.S, Presidential election hits a fever pitch, the persistently high cost of consumer goods is a huge talking point among the candidates and the voters.

That may be surprising to some, as the rate of inflation finally dropped below 3% this summer and, at its current 2.5%, represents a 73% drop from the 9.1% high that was reached in June 2022. But according to JD Power, the percentage of bank customers in the United States who are financially healthy[1] has only modestly improved, while the number of customers who say the cost of goods is increasing faster than they can afford has increased in the past month.

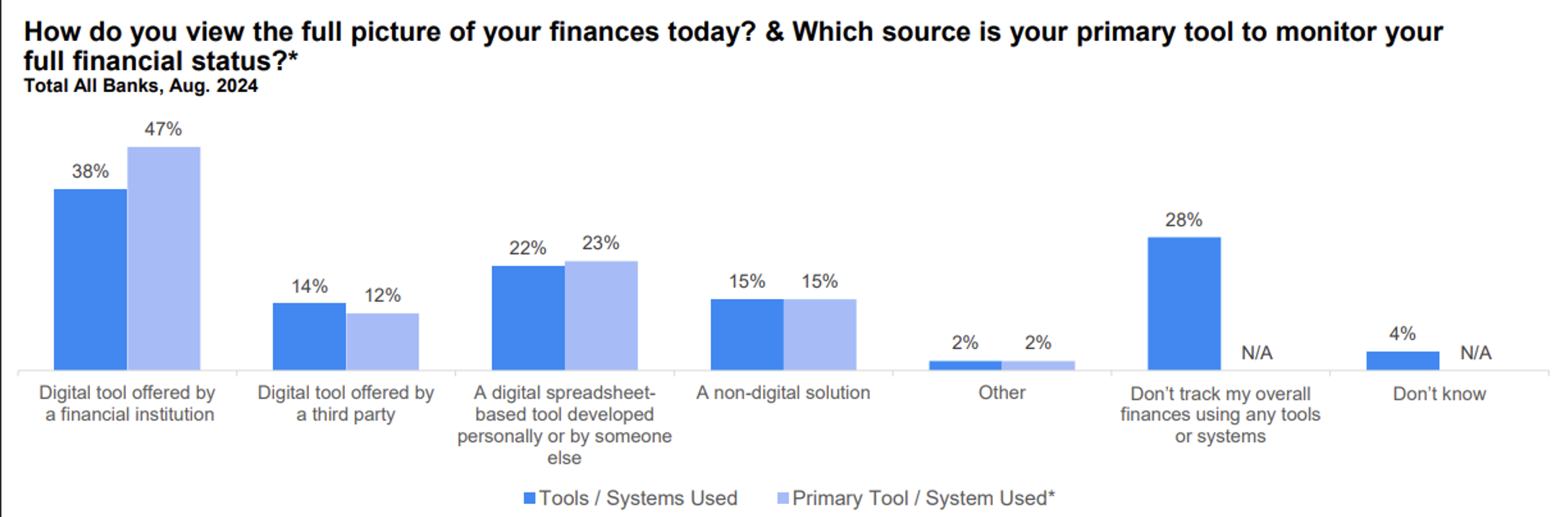

It’s a fact that is difficult to reconcile, leading some analysts to wonder just how reliable some customer feedback is. Notably, 28% of customers say they do not track their own financial status, leaving banks with the uphill task of building products and offering services to a clientele that is often in the dark about their actual situation and needs.

Inflation Becomes the Ultimate Enigma

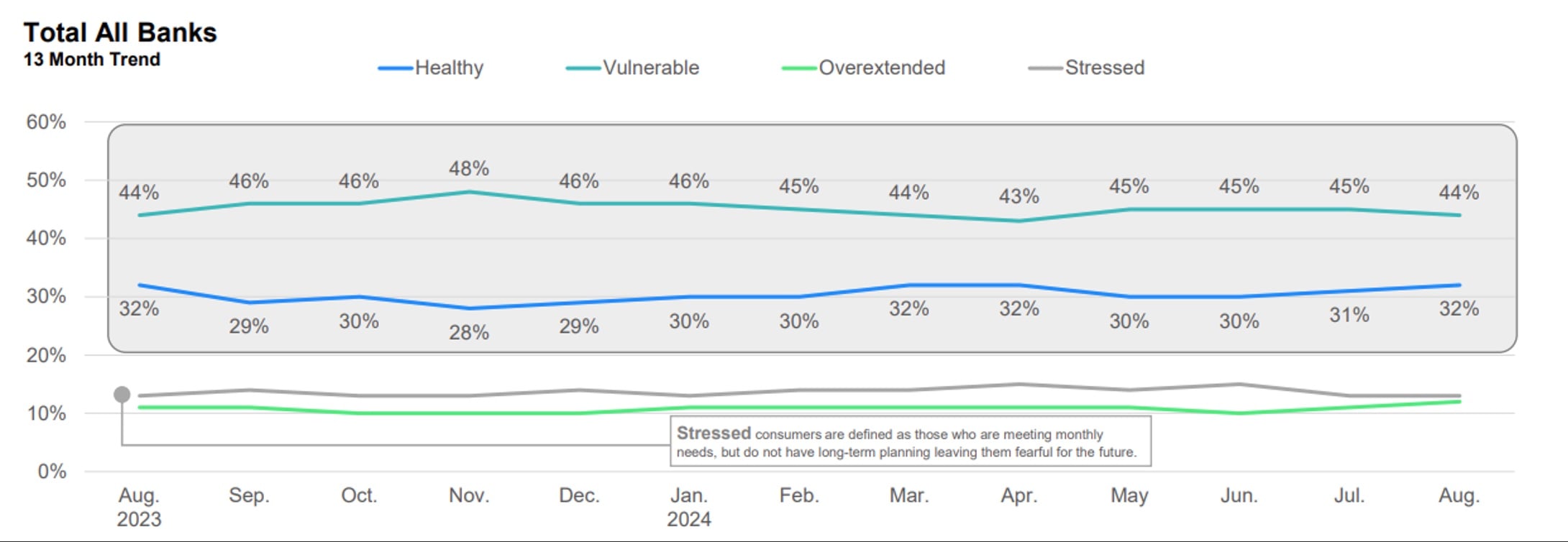

The number of customers who are financially healthy rose slightly to 32%, while 44% of bank customers fall into the vulnerable category.

For the first time in four months, the number of bank customers who say that the cost of goods is increasing faster than their income increased (68%). That rise comes amid the lowest inflation numbers in recent memory.

Relief Hard to Come By, But Lack of Tracking Breeds Confusion

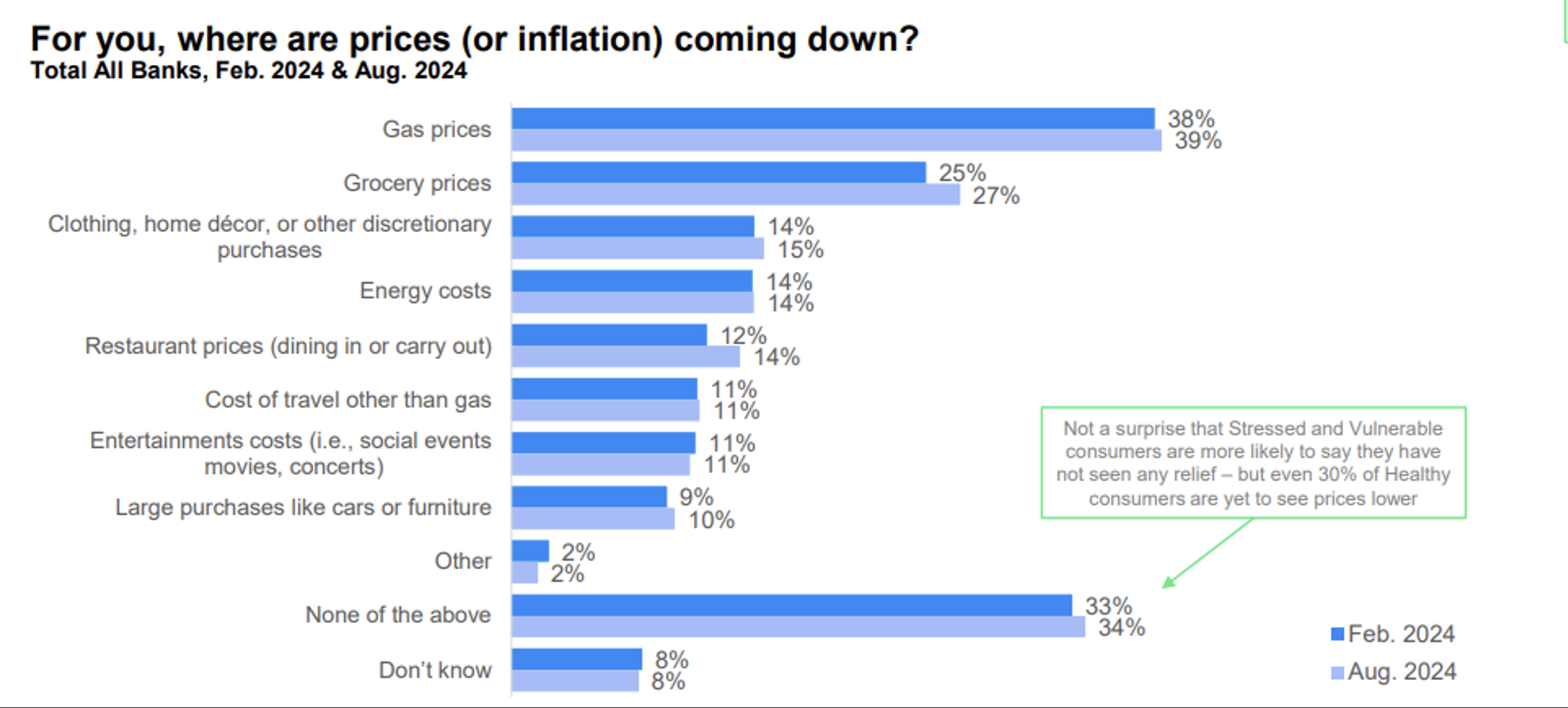

When asked about where they have experienced relief from inflation, customers express modest improvement from six months ago. Grocery and restaurant prices show the most improvement, but shockingly, 34% of customers say prices have not gone down for any goods. Those rates are highest among financially stressed and vulnerable customers, but even 30% of healthy customers say they have not felt any relief.

Even as customers continue to express struggles, there seems to be a disconnect between what customers feel and what they actually know. While some customers are using either banking digital tools or a personally made system, a surprisingly high 28% of customers admit that they do not track their finances with any digital tool or other system.

A Need for Clarity

Even with inflation easing, it is clear that customers are not feeling immediate relief. After being under duress for more than two years, financial health improvements are likely to lag inflation’s downward trend. That means that inflation is still a factor in many Americans’ day-to-day financial decisions.

For banks, this creates an interesting dilemma. With so many customers making choices, both financial and political, based on inflation, yet such a sizeable portion of them refusing to track their finances, it is difficult to build an outreach strategy. Banks will need a multi-pronged approach that incorporates financial literacy, vigilance, and planning to help customers out of the cycle of stress that they’ve been experiencing.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in August 2024. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.