Americans’ Financial Condition Continues to Deteriorate as Inflation Persists

Banking and Payments Intelligence Report

August 2022

Americans’ Financial Condition Continues to Deteriorate as Inflation Persists

As Americans enter the dog days of summer, they’re not just trying to beat the heat. Inflation has been an ever-present obstacle this year for most American banking customers’ financial health, and that trend persisted according to the latest JD Power data. Now, even financially healthy customers are feeling the sting; a disquieting trend as a potential recession looms.

According to the data, the proportion of those affected by inflation remains high, increasing to 70% of all retail bank customers. Somewhat surprisingly, the largest month-over-month increase is among Americans that are classified as financially healthy (3%).

What’s more, amid high inflation, Americans have begun to turn to credit cards to help shoulder their monthly burden. Unfortunately, it seems that some banking customers have chosen to carry higher credit card balances without knowing the extent to which that will affect their credit score: a sign that the after-effects of inflation may be felt by Americans for years to come.

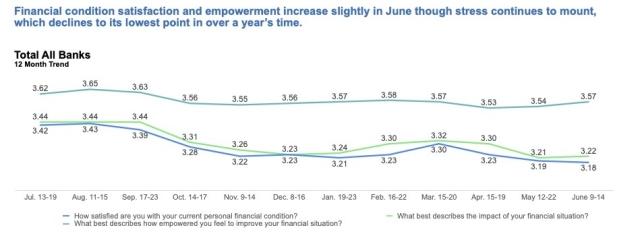

Even the Healthy Hurt

Recognition of inflation among Americans once again increased, but with a surprising twist: Customers whose financial situations are classified as healthy have the highest increase. It’s a sobering realization that the negative effects of inflation are mounting for all Americans.

As a result, customers indicate low levels of confidence in their ability to handle inflation, alongside sagging overall satisfaction with their financial conditions, which—for the second consecutive report—is at the lowest level since JD Power began tracking the metric. Despite these troublesome data points, however, the ratio of healthy to unhealthy customers remains relatively unchanged.

The Credit Score Mystery

One tactic that many bank customers have tried to combat inflation is leaning more heavily on credit cards. The mileage a customer may get out of that strategy varies, based on several factors that include card APRs, existing balances and an ability to make monthly payments. But one thing is certain: Carrying a higher balance on a card will affect a customer’s credit score.

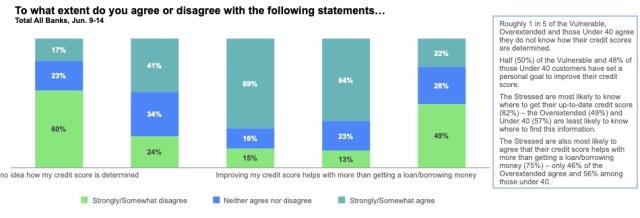

Alarmingly, a portion of customers are not aware of that equation. In fact, nearly one in five customers are unaware how their credit score is determined. The highest rate of respondents that are unsure are the vulnerable and under-40 populations.

While they may not exactly know how to do it, most customers know their credit score is important and are making improving it a priority. Customers whose financial health is stressed are most likely to agree that their credit score helps with more than getting a loan/borrowing money (75%) and, to that end, 41% of customers have a personal goal to improve their credit score in the next 12 months. That includes half of the vulnerable population and 48% of those under age 40. It’s an admirable goal, but it begs the question: What are banks doing to help their customers achieve it?

A Missed Opportunity

As we have seen time and time again, banks are offering budgeting and debt assistance, but customers just aren’t taking advantage of them. This month’s data illustrates the golden opportunity for banks to finally get that advice formula right.

One of the most challenging feats to accomplish in business is changing customer behavior. But in this instance, customers are ready to change. The problem is that they’re rudderless and unable to define where to direct their efforts. Banks need to be able to effectively steer customers into programs that can help with each unique individual financial situation.

While improving credit scores may be a short-term goal, it’s usually in the pursuit of a loftier one, whether that’s to qualify for a loan, purchase a home or grow a family. Banks need to understand customers’ motivation to find their best path forward. Those that do will be rewarded for their effort in the form of customers that are both more financially healthy and more likely to engage with that bank in the future.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in June 2022. It was authored by Jennifer White, senior director of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, creditworthiness, and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.