COSTA MESA, Calif.: 23 May 2019 — There is a crisis of confidence among U.S. retirement plan participants. According to the JD Power 2019 U.S. Retirement Plan Participant Satisfaction Study,SM released today, just 17% of plan participants say they feel “very confident” in their retirement preparedness. That number falls to 15% among Boomers1, who are currently entering retirement at a rate of roughly 10,000 per day2. To build that confidence, many retirement plan providers need to rethink their approach when it comes to both digital tools and human advisors.

“Understanding the drivers of confidence is critical for retirement plan providers because it’s directly linked to roll-in and rollover decisions,” said Mike Foy, Senior Director of Wealth Management Intelligence at JD Power. “Put simply, when retirement plan participants feel confident about their retirement, they are much more likely to bring assets to their primary plan from other sources, and to keep those assets with the provider after leaving their current job. To build that confidence, providers need to deliver an effective combination of high-quality human interaction, useful online tools and thoughtfully designed digital self-service options.”

Following are some key findings of the 2019 study:

- Building confidence can pay off: Overall satisfaction with retirement plan providers is nearly 220 points higher (on a 1,000-point scale) when plan participants are “very confident” in a majority of the 11 areas related to retirement measured in the study vs. those who are “not confident at all” in at least one area. The percentage of participants who say they “definitely will” keep assets with their provider (either in the plan or a rollover) after leaving their job (46%) and have rolled in assets to their primary firm (47%) is highest when participants identify as “very confident” in a majority of areas.

- More robust mobile engagement is critical: Most retirement plan participants use a combination of website, mobile and phone channels to interact with their plan providers, but when awareness and/or usage of mobile capabilities are limited, providers are missing an opportunity to both increase participant satisfaction and reduce dependency on more expensive service channels. Satisfaction increases dramatically among participants who actively use the mobile channel, not only for reviewing information but for transaction and communication.

- Retirement plan providers must deliver a great digital experience but can’t ignore human interaction: Retirement plan participants have the highest levels of overall satisfaction (877) and confidence in a majority of areas (46%) when they are actively engaged with their retirement plan provider across multiple channels, including online retirement tools, digital self-service options and professional advisors.

Study Rankings

Charles Schwab ranks highest in group retirement plan satisfaction in the large plan segment, with a score of 821. Nationwide (811) ranks second and Bank of America (809) ranks third.

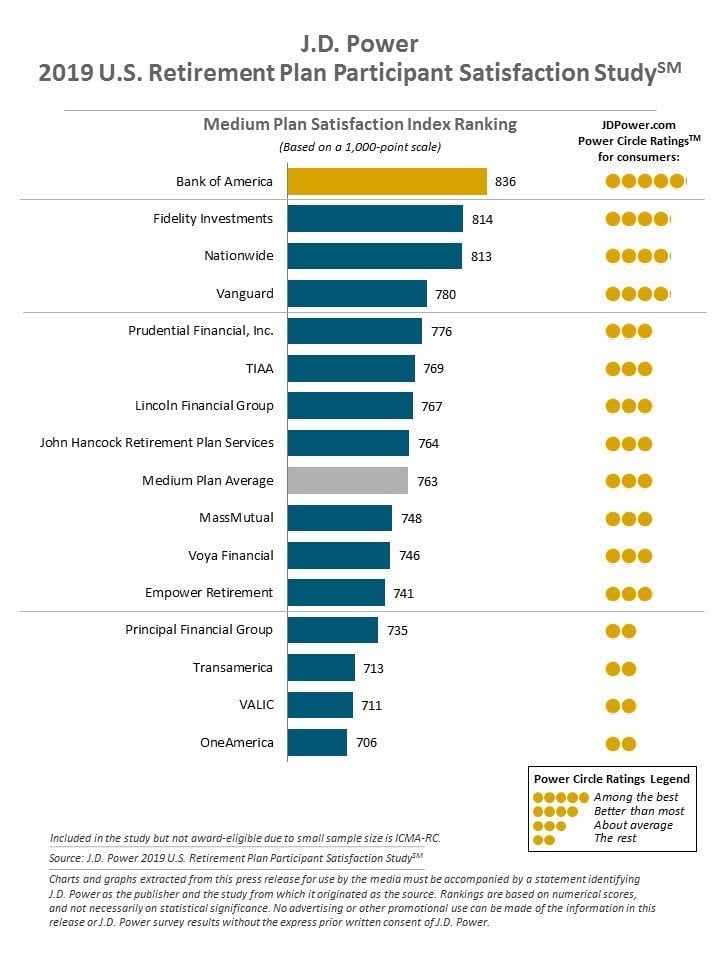

In the medium plan segment, Bank of America ranks highest, with a score of 836. Fidelity Investments (814) ranks second and Nationwide (813) ranks third.

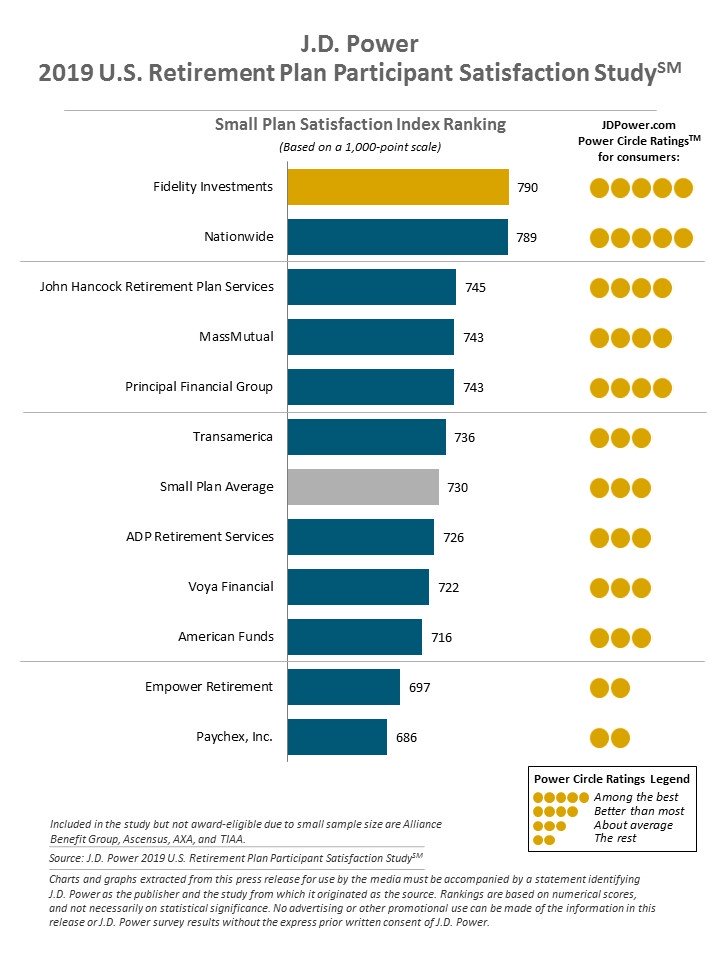

In the small plan segment, Fidelity Investmentsranks highest, with a score of 790. Nationwide (789) ranks second and John Hancock Retirement Plan Services (745) ranks third.

The U.S. Retirement Plan Participant Satisfaction Study, now in its second year, evaluates participant satisfaction with providers of group retirement plans, such as 401(k)s, based on six factors: interaction across live and digital channels; investment and service offerings; fees and expenses; plan features; information resources; and communications. Plan providers are ranked in three categories based on their overall mix of business in terms of average plan size. The study is based on responses of 8,332 retirement plan participants and was fielded in February-March 2019.

For more information about the U.S. Retirement Plan Participant Satisfaction Study, visit https://www.jdpower.com/business/resource/us-group-retirement-satisfaction-study.

JD Power is a global leader in consumer insights, advisory services and data and analytics. These capabilities enable JD Power to help its clients drive customer satisfaction, growth and profitability. Established in 1968, JD Power has offices serving North America, South America, Asia Pacific and Europe.

Media Relations Contacts

Geno Effler, JD Power; Costa Mesa, Calif.; 714-621-6224; [email protected]

John Roderick; St. James, N.Y.; 631-584-2200; [email protected]

About JD Power and Advertising/Promotional Rules: www.jdpower.com/business/about-us/press-release-info

1JD Power defines generational groups as Pre-Boomers (born before 1946); Boomers (1946-1964); Gen X (1965-1976); Gen Y (1977-1994); and Gen Z (1995-2004). Millennials (1982-1994) are a subset of Gen Y.

2Source: Benefits Pro, Jan. 8, 2019, “The Baby Boomer Generation is Starting to Retire – And No One is Prepared,” https://www.benefitspro.com/2019/01/08/the-baby-boomer-generation-is-starting-to-retire-a/?slreturn=20190417135157