WESTLAKE VILLAGE, Calif.: 16 November 2015 — Overall mortgage customer satisfaction has increased this year as lenders have focused on developing functional digital channels and improving operational efficiency. Despite this overall increase in satisfaction, mortgage lenders are under increased pressure from new loan disclosure regulations that could increase the time it takes to get a home loan while also facing increased competition from non-traditional lenders, according to the JD Power 2015 U.S. Primary Mortgage Origination Satisfaction StudySM released today.

The study measures customer satisfaction with the mortgage origination experience in six factors (listed in alphabetical order): application/approval process; interaction; loan closing; loan offerings; onboarding; and problem resolution. Satisfaction is calculated on a 1,000-point scale.

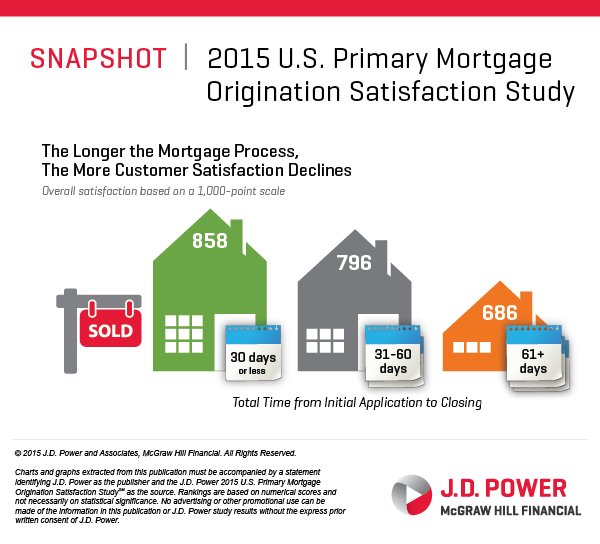

Overall customer satisfaction with mortgage origination averages 793 in 2015, an increase of 7 points from 2014. The increase in satisfaction is driven by a 22 point gain in the application and approval process factor, influenced by improved perceptions of the speed of the loan process. When loans close earlier than promised, satisfaction is significantly higher (866), compared to when loans close as expected (821) and when it takes longer than expected (658).

The study also finds that overall satisfaction with several mortgage application-related activities, such as completing an application (799), submitting documents (804) and receiving status updates (811) is markedly higher among customers who used digital communication channels versus those who communicated via mail and fax (753, 766, and 770, respectively).

The links between the perception of mortgage processing speed and efficiency and overall customer satisfaction are particularly noteworthy in light of new TRID (TILA RESPA Integrated Disclosure[1]), a.k.a. “know before you owe” regulation, which went into effect in October 2015. This law has the potential to increase the mortgage timeline which poses a significant challenge for lenders when serving home buyers across all generations, but could be particularly challenging when dealing with Millennials (ages 18-34) who are technically savvy, always connected to the Internet and noted as being capricious consumers.

“While a lot of effort has been placed on ensuring compliance with new regulations, it is imperative that lenders improve their education and communication about the impact of these changes or risk losing customers,” said Craig Martin, director of the mortgage practice at JD Power. “Effective communication remains one of the most important aspects of a satisfying mortgage experience, especially if the process is taking longer than it has historically. As the number of Millennial home buyers continues to rise, lenders must be ready to meet their expectations. This generation is highly digitally connected, so ongoing communication and transparency via the channels they prefer, particularly mobile, are vital.”

Following are some of the key findings in this year’s study:

- Communication Impacts Satisfaction: Communication throughout the loan process mitigates dissatisfaction with a longer timeline. When the loan process takes more than two months, satisfaction is 686. However, when an accurate time frame estimate and proactive updates are provided in that same scenario, satisfaction is 859.

- Millennials Seek Guidance: With Millennials now accounting for the largest share of loan originations over the last two years[2], it is notable that nearly 4 in 10 (37%) millennial customers indicate that the origination process was not completely explained to them, and 58% indicate their options, terms and fees were not completely explained.

- Effective Loan Representatives are Vital: Those loan reps who engage customers, build trust and ensure that borrowers understand each step of the process can mitigate the negative impact on satisfaction due to missing closing dates (764 missed date/effective representative vs. 511 missed date/ineffective representative).

- Loans are Closing Sooner: The percentage of applications and approvals that close earlier than promised has increased to 35% in 2015 from 31% in 2014.

- Satisfying Experience Leads to Recommendations and Loyalty: Providing an outstanding mortgage origination experience can generate high levels of advocacy and retention. The study finds that 71% of highly satisfied customers (overall satisfaction scores of 900 or higher) say they “definitely will” recommend their lender, and 76% say they “definitely will” consider reusing the same lender for their next home purchase. In comparison, only 5% of dissatisfied customers (scores of 699 or less) say they “definitely will” recommend and 8% say they “definitely will” consider reusing the lender.

2015 U.S. Primary Mortgage Origination Satisfaction Rankings

Quicken Loans ranks highest in primary mortgage origination satisfaction for a sixth consecutive year, with a score of 850, an increase of 15 points from 2014. Quicken Loans performs particularly well in all six factors. Fifth Third Mortgage ranks second with a score of 812, followed by Bank of America and BB&T (Branch Banking & Trust Co.) in a tie at 811 each.

The 2015 U.S. Primary Mortgage Origination Satisfaction Study is based on responses from 4,666 customers who originated a new mortgage or refinanced within the past 12 months. The study was fielded in two waves: February – March and July – August 2015.

For more information about the 2015 U.S. Primary Mortgage Origination Satisfaction Study, visit

http://www.jdpower.com/resource/us-primary-mortgage-origination-satisfaction-study

Media Relations Contacts

Jeff Perlman; Brandware Public Relations; Woodland Hills, Calif.; 818-317-3070; [email protected]

John Tews; Troy, Mich.; 248-680-6218; [email protected]

About JD Power and Advertising/Promotional Rules www.jdpower.com/about-us/press-release-info

About McGraw Hill Financial www.mhfi.com

[1] For information about TRID visit http://www.consumerfinance.gov/regulatory-implementation/tila-respa/