Banking and Payments Intelligence Report

June 2022

Inflation is Causing Americans to Make Trade-Offs, Both Large and Small

For decades, social commentators have been discussing “The Two Americas.” The divide can be represented by conflicting ideologies, race or religion. As wealth disparity has grown over time, the term has also been used to describe the discrepancies between the lives of those with means and those without.

According to JD Power data, it’s clear the country is indeed split into two very different worlds when it comes Americans’ financial health and their attitudes to the current economic landscape.

As inflation continues to be a persistent problem, the high price of consumer goods has been a thorn in the side of Americans everywhere. But when asked what worries them the most, responses from banking customers vary widely, based on the financial health[1] of each individual customer.

Concerns Mount Over Product Availability and Cost

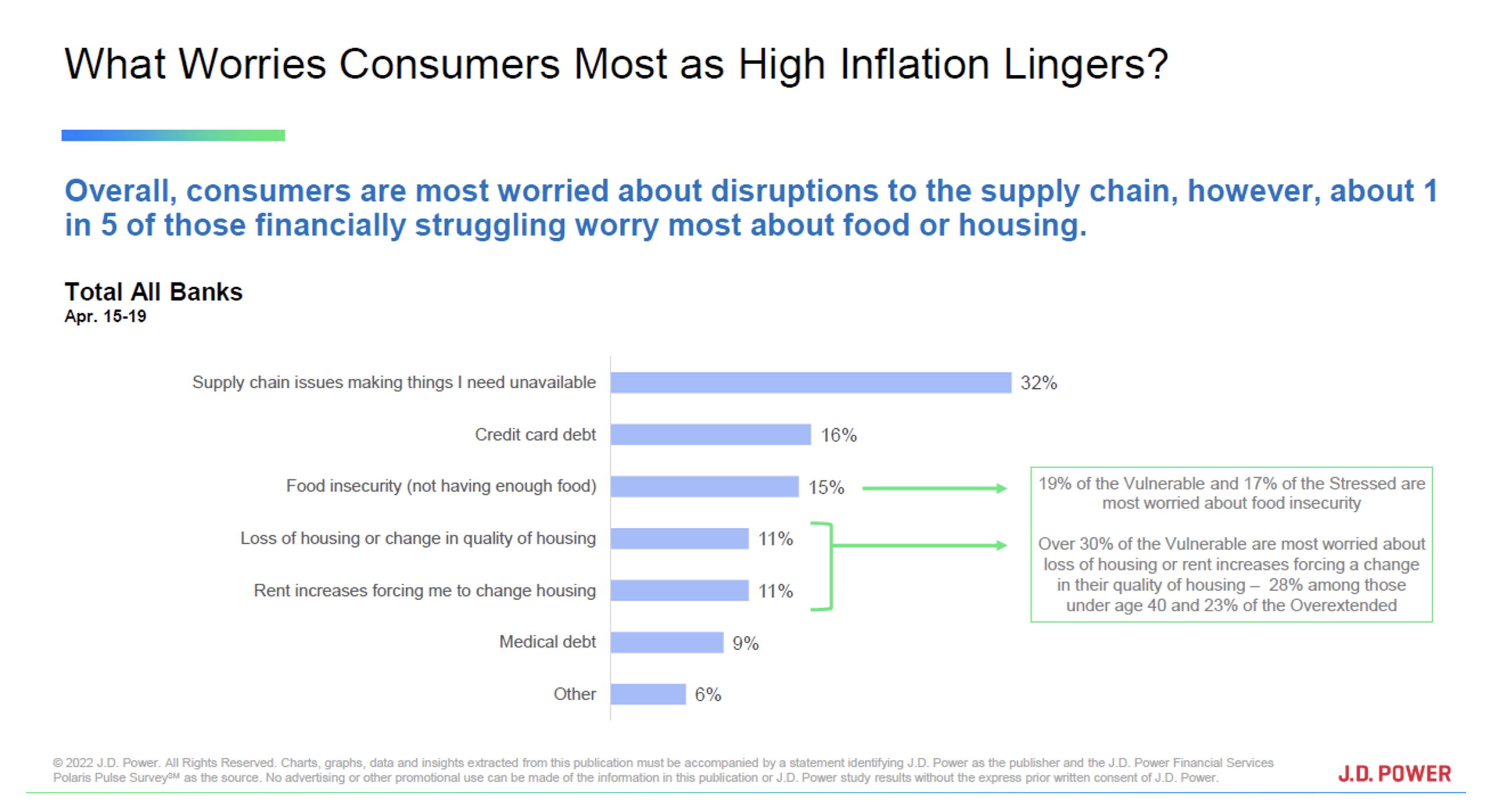

The bifurcation is most evident in how customers describe their biggest financial concern. While many Americans are concerned about the rising costs of essential goods, many others appear to be more concerned about the availability of them. In fact, disruptions to the supply chain that would prevent access to the products consumers need and want most is currently the top worry of American banking customers.

However, for those in more precarious states of financial health, the worries are decidedly more significant. Among those categorized as financially vulnerable, a group that accounts for roughly 40% American banking customers, nearly 1 in 5 bank customers indicate food insecurity is their greatest concern. What’s more, 31% of vulnerable and 23% of overextended customers say their greatest worry is a loss or change in quality of housing. Consumers aged 40 and older are more likely to list housing as a significant worry than those under age 40. Overall, 28% of consumers spend time worrying about whether they have enough food, and this worry distracts employees an average of 15 hours a week.

Financially Vulnerable Americans Start Making Meaningful Changes

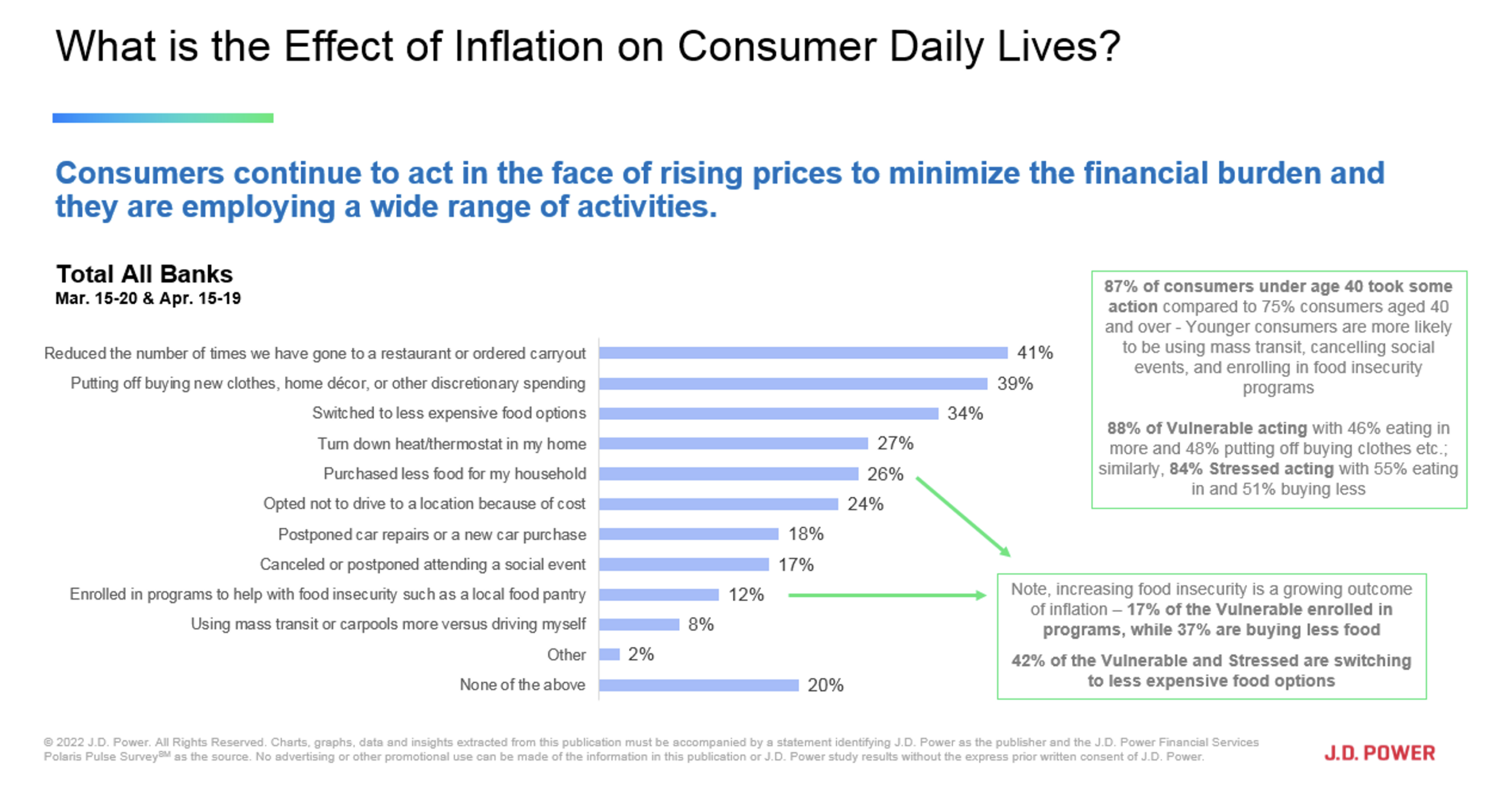

Against this backdrop of mounting financial concern, many Americans are taking measures to curb spending. The most common measure taken by customers to combat the rising cost of goods is reducing the amount of times they visit a restaurant or order take-out (41%).

Putting off buying new clothes (39%), switching to less expensive food option (34%), and turning down the thermostat in their home (27%) are the next-most common responses. This suggests that a large swath of Americans aren’t necessarily doing without some of their luxury items; rather, they’re just partaking in them less—a fact that could account for credit card debt ranking so high on the list of customer concerns.

Still, there are enough Americans that have been forced to make major sacrifices—like buying less food for their home (26%) and enrolling in local food pantry programs (12%)—that it is clear many customers are teetering on the edge. As banks begin to appraise this shaky financial terrain, they need to achieve a level of understanding to help see their customers through to the other side.

Banks and Employers in Position to Help

As we reported in the JD Power 2022 U.S. Retail Banking Satisfaction Study,SM the one factor that does heavily influence bank customer experience in this environment is the bank’s ability to “support the customer during challenging times.” We found that customer satisfaction with retail banks rises 155 points (on a 1,000-point scale) when customers indicate that their bank supports them during challenging economic times.

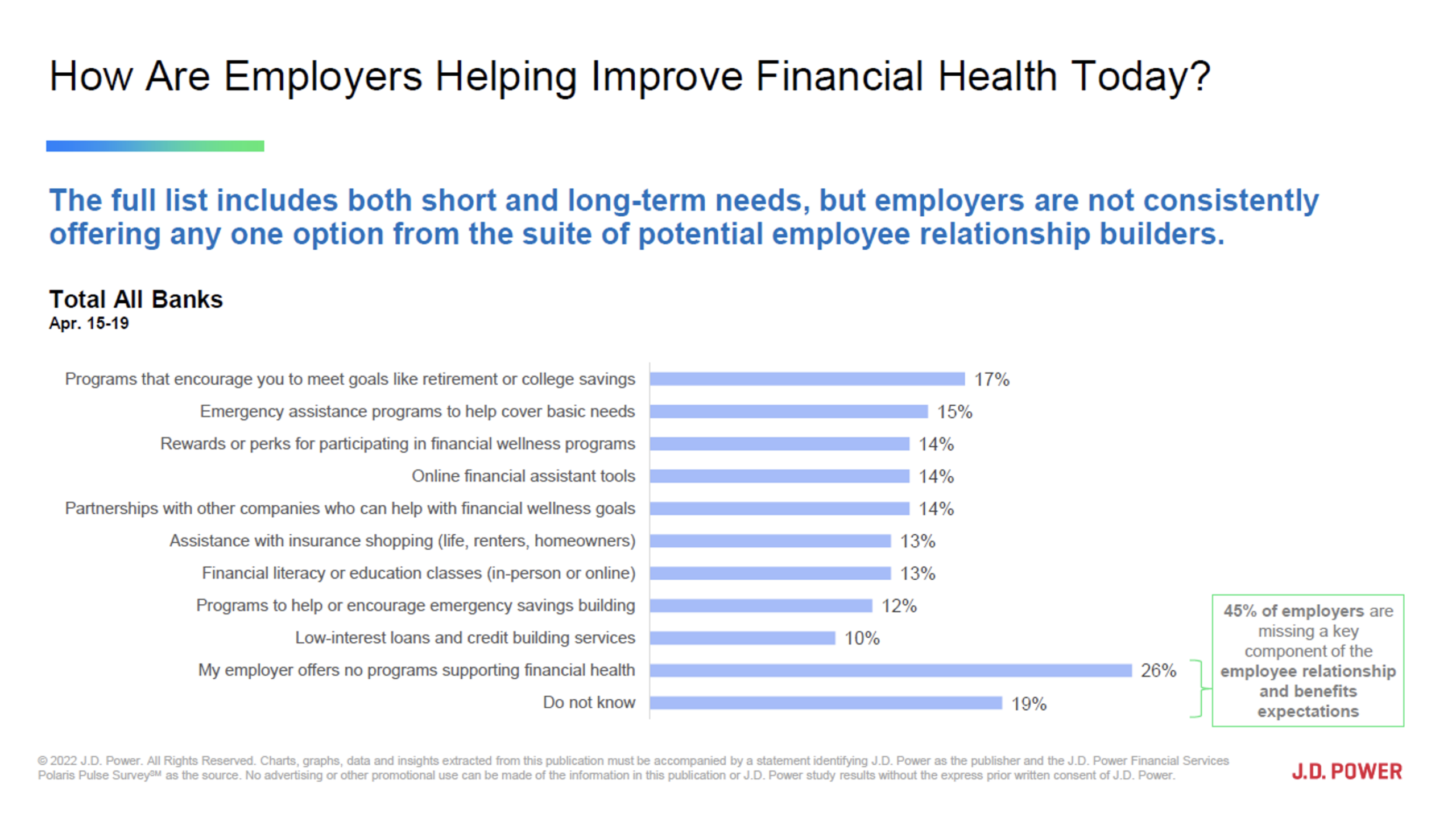

As banks make a concerted push on customer retention, they need to find ways to tailor their communications and services to reflect a level of understanding of where their customers are on the financial spectrum. That includes partnering with employers, who are currently positioned as one of the most integral and involved entities in a customer’s life. Americans are craving employer intervention, yet 45% of all large employers do not do anything to support their employees’ financial health.

For banks to earn the kind of loyalty that they hope to receive from their customers, they must meet Americans where they are. That includes getting employers involved, connecting with customers and delivering the right combination of financial incentives, personalized financial advice, hands-on help with problem resolution and guidance on how to grow their money.

Find out More

This Banking and Payments Intelligence Report is based on responses from 4,000 retail bank customers nationwide and was fielded in April 2022. It was authored by Jennifer White, senior consultant of banking and payments intelligence at JD Power. Please contact us at the numbers below to connect with Ms. White or to learn more about the underlying research.

Media Contacts

Brian Jaklitsch; East Coast; 631-584-2200; [email protected]

Geno Effler, JD Power; West Coast; 714-621-6224; [email protected]

[1] JD Power measures the financial health of any consumer as a metric combining their spending/savings ratio, credit worthiness and safety net items like insurance coverage. Consumers are placed on a continuum from healthy to vulnerable.